Valuation guide

SaaS Acquisition Multiples: What Buyers Really Pay (And Why)

A few years ago, I sold a company called Zencast. The buyer offered 3.48X earnings on an all-cash, next-day exit. No equity rollover. No drawn-out earnout clauses. Just cash in the bank immediately.

At the time, I remember thinking: "Is that good? Should I push back?" So I started digging into what acquisition multiples actually meant—and discovered something most founders get wrong.

The answer wasn't just about the multiple itself. It was about which multiple—earnings vs. revenue, the deal structure, and a critical macroeconomic reality: when interest rates are high, debt is expensive, and acquisition multiples compress. Right now, in 2025, we're in a compressed multiple environment. That's not a personal failure on your part as a founder. It's just the market.

Whether you're evaluating an acquisition offer, planning your exit strategy, or trying to understand why your SaaS company is worth what it's worth, you need to understand SaaS acquisition multiples—and understand them clearly, because the numbers can be deceptively simple on the surface while the reality underneath is far more nuanced. Understanding SaaS valuation multiples is particularly crucial since they determine not just your exit price, but also how buyers evaluate risk and structure deals.

In this post, we'll walk through:

- How SaaS valuation multiples actually work—and the critical distinction between earnings multiples and revenue multiples

- Where SaaS valuation multiples stand in 2025 and why the macro environment matters

- What actually drives multiples—from growth rate to deal structure

- A critical warning about AI-powered SaaS and durability risk

- How to actually improve your multiple before exit

- Why the $500M ARR inflection point changes everything

If you're a founder considering selling, fundraising on valuation, or just trying to understand your company's value: this is the framework you need.

Understanding SaaS Acquisition Multiples

Let's start with the basics, because a lot of founders don't actually know what "multiple" means in the context of an acquisition. SaaS valuation multiples are the primary framework buyers use to determine what they'll pay—yet most founders misunderstand which type of multiple applies to their business.

An acquisition multiple is simple in theory: it's the acquisition price divided by a company's annual financial metric. The formula looks like this:

Simple, right? But here's where most founders go astray: not all multiples are created equal.

The Critical Distinction: Earnings Multiples vs. Revenue Multiples

When a buyer evaluates your SaaS company, they're typically using one of two approaches:

Revenue Multiples (ARR or MRR-based)

This is the simpler, cruder approach. The buyer simply looks at your annualized recurring revenue and multiplies it by some factor.

Example: A company with $500K ARR acquired at a 4X revenue multiple = $2M acquisition price.

Revenue multiples are more common in the early-stage SaaS world (pre-profitability) because, well, revenue is the only metric you have. A burning startup isn't going to have positive earnings.

In 2025, typical SaaS valuation multiples on an ARR basis range from 2.5X to 6X, depending heavily on growth rate, customer durability, and deal structure. These SaaS valuation multiples are significantly lower than the inflated multiples seen during the 2020-2021 ZIRP era.

Earnings Multiples (EBITDA or Net Income-based)

This is the more sophisticated approach—and it's what sophisticated buyers prefer because it captures the actual cash the company generates.

Example: A company with $300K annual earnings acquired at a 4X earnings multiple = $1.2M acquisition price.

Earnings multiples matter because they account for your unit economics. Two $1M ARR companies can be valued very differently if one has 10% net margins and the other has 50% net margins.

In 2025, healthy SaaS companies see earnings multiples in the 3.5X to 6.5X range (for 30% YoY growth) and 4X to 5X range (for slower-growing, stable, mature SaaS). The range depends heavily on whether the revenue is truly durable and whether the buyer has confidence in your business model.

Why This Matters: The Zencast Example

When I sold Zencast, the buyer offered a 3.48X earnings multiple on an all-cash, next-day basis. That's on the lower end of the current market range. But here's the thing: I accepted it because of how the deal was structured.

The deal included:

- All cash upfront (no equity rollover, no waiting around)

- No earnout constraints (I wasn't at risk of losing money if the business performed differently post-exit)

- A personal guarantee on the buyer's assets

That personal guarantee was unusual. It meant the buyer was putting their personal assets behind the deal, giving me extra security. That's worth something. In return, I accepted a multiple on the lower end of the range because the certainty and deal structure were worth more to me than chasing 0.5X additional multiple with an earnout that might not pay out.

The lesson: Don't just look at the multiple in isolation. The structure of the deal—how you get paid, what risks you're taking post-exit—fundamentally changes whether a "low" multiple is actually a bad deal.

One More Thing: Revenue Share & Alternative Structures

Not all acquisitions fit the clean "X multiple" model. Many deals—especially at the micro-SaaS and vertical SaaS level—use hybrid structures:

- Revenue share: You get a percentage of revenues going forward (instead of a lump sum)

- Earnout: You get a base amount now, plus additional cash if the company hits certain milestones (growth, retention, etc.)

- Seller financing: The buyer can't pay 100% upfront, so they pay you over time

- Mixed structures: A combination—like a lump sum + revenue share + personal guarantee

Castanet was acquired using a mixed structure: lump sum cash payments + ongoing revenue share, which kept the reported multiple lower but provided more security and upside for the founder. In this case, the lower multiple reflected the unique structure, not a bad deal.

Bottom line: When evaluating an offer, look at the effective value you're getting across all deal terms, not just the headline multiple.

A Quick Warning: Earnings Multiples and AI-Powered SaaS

If your SaaS is built on top of an LLM API—ChatGPT, Claude, Google's models—your earnings multiple might look attractive on paper, but it's hiding a critical risk: durability.

OpenAI, Google, and Anthropic are all rapidly building features that SaaS startups built as separate products. When Google integrated email into Workspace, it destroyed the standalone email SaaS market. When OpenAI added image generation to ChatGPT, it disrupted Midjourney's market. This pattern repeats constantly.

A buyer looking at your earnings multiple needs to ask: "How long until the foundation model company itself builds this feature?" If the answer is "18 months," then your earnings today might evaporate tomorrow. A savvy buyer will discount that multiple significantly, or walk away entirely.

We'll dive deeper into evaluating AI wrapper durability in a dedicated section below. For now: be skeptical of any AI wrapper's earnings multiple without a credible answer to the durability question.

Historical Trends & Data: Where We Are in 2025

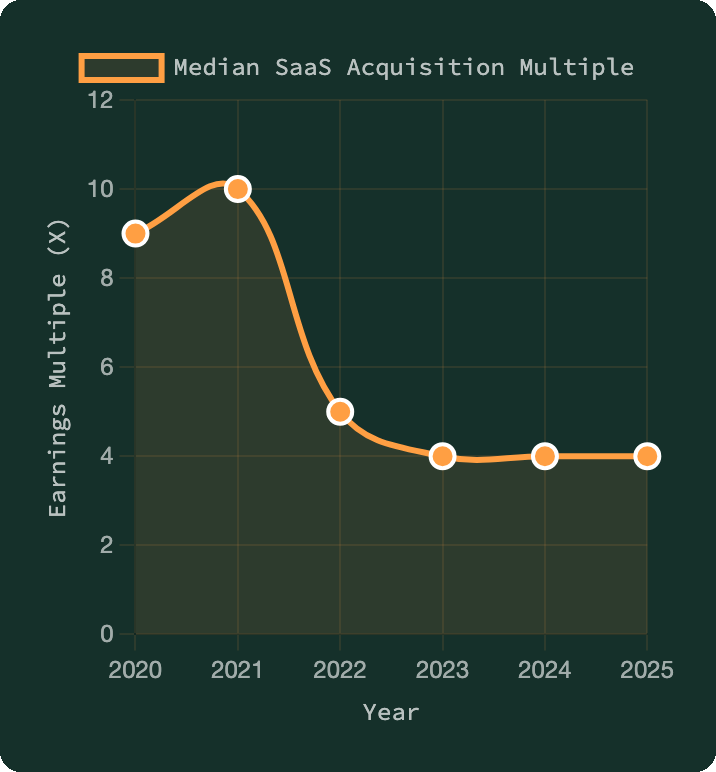

To understand where SaaS acquisition multiples are right now, you need to understand where they've been. And the last 5 years have been a wild ride.

The ZIRP Era and the Collapse

From roughly 2020-2021, we lived through an unprecedented period: ZIRP, or "Zero Interest Rate Policy." The Federal Reserve kept interest rates near zero. Money was free. Debt was cheap.

When debt is cheap, it's easy for larger companies to finance acquisitions with borrowed money. That abundance of capital pushed acquisition multiples to historic highs. SaaS companies that would have sold for 4-5X multiples in a normal environment were fetching 8-10X or more. Some strategic acquisitions hit 12X+.

Founders understandably got used to that environment. They expected it would continue.

It didn't.

Starting in 2022, the Fed began aggressively raising interest rates to fight inflation. Debt became expensive. Acquisition multiples compressed. Fast.

SaaS acquisition multiples peaked in 2021 during ZIRP, crashed in 2022-2023, and have stabilized in 2024-2025 at 4X—roughly 60% below ZIRP highs.

2023-2025: Stabilization, Not Recovery

Here's what's important to understand right now: multiples have stabilized, but they're not recovering to ZIRP levels.

The current environment shows:

- Fast-growing SaaS (30%+ YoY ARR growth): 3.5X to 6.5X earnings multiples, depending on durability and margins

- Stable/mature SaaS (5-20% YoY growth): 4X to 5X earnings multiples

- Slow/declining SaaS: No longer valued on revenue or earnings multiples; instead valued on Discounted Cash Flow + liquidation assets

These are significantly lower than the 2021 peaks, but they're realistic and sustainable given current economic conditions.

Why Multiples Won't Bounce Back Soon (And What It Means For You)

Here's the uncomfortable truth: acquisition multiples are unlikely to recover to 2021 levels for years, and it has everything to do with macro policy, not your company's performance.

Here's why:

1. The inflation problem requires a debt-unfriendly solution. The U.S. federal government is running massive budget deficits. The traditional way to "solve" that problem without raising taxes is inflation. And when inflation is high, the Federal Reserve has to raise interest rates to combat it. High rates make debt expensive.

2. Acquisition financing relies on cheap debt. When a large company buys another company, they often finance the deal with corporate debt. If that debt is expensive (high interest rates), the math breaks down. A buyer can't pay 6X multiples with 7% debt financing; the ROI doesn't work.

3. Your exit multiple is downstream of the buyer's cost of capital. If you're hoping for a 6X multiple but the buyer's cost of capital is 8%, they'll offer 3-4X instead because that's what makes financial sense for them.

This is why founders who sold in 2021 at 10X multiples, and then watch their peer companies selling at 4X multiples, shouldn't feel bad. It's not a reflection of your company getting worse. It's a reflection of the macro environment.

The timeline for multiples to recover meaningfully depends on when—and if—inflation stabilizes and the Fed can lower rates sustainably. That's not something any of us can predict with certainty, but it's not happening in 2025.

By Company Type & Stage

Multiples also vary significantly by company type and maturity:

Horizontal PLG (Product-Led Growth): Higher growth potential, but also more competition and higher burn rates historically. Multiples tend toward the middle: 4X-6X earnings for healthy growth scenarios.

Vertical SaaS: Focused customer base, often higher net margins, lower churn. These command a slight premium: 4.5X-6.5X earnings for 25%+ growth, stable churn.

Enterprise SaaS: Long sales cycles, high ACV, lower churn. Also command a premium when they show expansion revenue and low net negative churn. Range: 5X-6.5X earnings.

Micro-SaaS / Bootstrap SaaS: Lower absolute revenue but often high margins and low burn. These are increasingly attractive to individual buyers and smaller PE firms. Multiples: 3.5X-5X earnings, heavily dependent on durability.

Notable Recent Acquisitions (2024-2025)

To ground this in reality, here are a few recent public acquisitions and their approximate multiples:

| Company | ARR | Exit Price | Multiple | Why This Multiple? |

|---|---|---|---|---|

| Predictology | $445K | $720K | 1.6X | Mature 10-year business with database moat, but slower growth justifies lower multiple |

| Median Cobrowse | $75K | $280K | 3.7X | Bootstrapped micro-SaaS with solid fundamentals and stable revenue |

| Userflow | $4.6M | $60M+ | 13X | Strategic buyer (Beamer) saw major synergies. Financial buyer would pay 5-7X only |

Important caveat: These are not representative of the market you're operating in if you're at the mega-acquisition level. A $1M-$5M ARR SaaS exit will not follow the same multiples as a $500M+ ARR company with massive strategic value to a Fortune 500 acquirer. We'll dig into that distinction in depth later.

What Actually Drives Your Acquisition Multiple

Now that you understand what multiples are and where they stand in 2025, the question is: what determines YOUR company's specific multiple?

It's not random. Buyers follow a repeatable framework when evaluating SaaS companies. Let's break down the key factors.

1. Growth Rate (The Biggest Driver)

Growth rate is the single biggest driver of acquisition multiples. A company growing at 30% YoY is fundamentally more valuable than a company growing at 5% YoY, assuming similar margins.

The 2025 reality:

- 30%+ YoY growth: 3.5X-6.5X earnings multiple (the range depends on durability; see AI wrapper warning below)

- 20-30% YoY growth: 3.5X-5X earnings multiple

- 10-20% YoY growth: 3X-4.5X earnings multiple

- Below 10% YoY growth: 2.5X-3.5X earnings multiple (or DCF-based valuation)

| Annual Growth Rate | Earnings Multiple Range | What This Means |

|---|---|---|

| 30%+ YoY | 3.5X - 6.5X | Rapid growth commands premium; wide range due to durability factors |

| 20-30% YoY | 3.5X - 5X | Solid growth trajectory; attractive to most buyers |

| 10-20% YoY | 3X - 4.5X | Steady growth; mature market or slower scaling |

| Below 10% YoY | 2.5X - 3.5X | Stagnant growth; DCF valuation likely used instead |

Why? Because a buyer is essentially paying for future cash flows. If your company is growing fast, there's more cash flow ahead. If it's stagnant, there's less.

2. Unit Economics and Profitability (The Legitimacy Test)

A buyer wants to see that your business actually makes money, or has a clear path to profitability. This affects the multiple significantly.

Key metrics buyers evaluate:

- Net Retention Rate (NRR): Are your existing customers expanding, staying flat, or churning? NRR above 100% (expansion revenue) is attractive and can justify a higher multiple. NRR below 100% is a red flag.

- Gross Margin: A 80% gross margin SaaS business is more attractive than a 40% margin business, all else equal. Higher margins mean more cash to spend on growth and retention.

- CAC Payback Period: How long does it take to recoup your customer acquisition costs? Under 12 months is good. Over 24 months is risky for a buyer.

- Churn Rate: A buyer looks at both logo churn (% of customers leaving) and revenue churn (% of revenue lost to churn). High churn is a multiple killer.

- Profitability: Are you EBITDA positive? Pre-revenue? Bleeding cash? A profitable business commands a higher multiple than a growing-but-burning business.

Real example: In 2024, an anonymous call tracking and analytics SaaS sold on Flippa with $304K ARR and 89% profit margin. That high margin justified a higher multiple than a comparable-revenue company with 50% margins would receive.

3. Customer Concentration (The Risk Factor)

If 30% of your revenue comes from one customer, buyers get nervous. If your top 10 customers represent 70% of revenue, that's a red flag.

Why? Because if even one large customer leaves post-acquisition, the buyer's ROI collapses. This drives multiples down significantly—sometimes by 1-2X or more.

Ideal buyer target: No single customer is more than 5-10% of revenue. Top 10 customers are less than 50% of revenue.

4. Technology Debt and Durability

Is your codebase a mess? Built on outdated frameworks? Running on technology that's a decade old? Buyers factor this in.

Healthy codebase (automated tests, modern stack, documented): Full multiple range

Some technical debt (missing tests, older frameworks but functional): 10-20% discount to multiple

Significant debt (no tests, legacy stack, hard to modify): 30-50% discount to multiple (or buyer walks away)

Tech debt matters because the buyer will inherit it. If they need to rewrite your entire backend post-acquisition, that's millions in hidden costs that they'll subtract from the purchase price.

5. Deal Structure (This Actually Matters A Lot)

We touched on this with Zencast and Castanet, but it's worth emphasizing: the way the deal is structured can change your effective multiple by 1-2X.

All-cash, no-contingencies deal: You might accept a lower headline multiple (3.5X) because you get certainty and zero risk post-exit. Castanet and Zencast are examples of this trade-off.

Earnout-heavy deal (50% at close, 50% over 2 years): You might get a 5X headline multiple, but you're taking on risk. If the business doesn't perform post-acquisition, you lose money. Effective multiple might be 3X if you don't hit earnout targets.

Seller financing (buyer pays you over time): You're financing their acquisition, which reduces your effective multiple and increases your risk. Usually only acceptable if the headline multiple is significantly higher (5.5X+) to compensate.

Revenue share model (ongoing payments): You get lower upfront payment (lower headline multiple) but ongoing revenue. Could be better or worse depending on how long you want to be involved post-exit.

As a founder, you need to evaluate the effective value you're receiving across all deal terms, not just the headline multiple.

6. Market Conditions and Buyer Type

The same company might sell for different multiples depending on who's buying.

Strategic buyer (larger company in your space): Usually willing to pay higher multiples because they see synergies (customer overlap, integrated features, etc.). Might pay 5-7X earnings.

Financial buyer / PE firm: Evaluating purely on financial return. More conservative multiples, typically 3-5X earnings. Needs to work backward from their target IRR (internal rate of return).

Individual buyer / micro-acquisition: Variable. Might be a competitor wanting to eliminate you, willing to overpay. Or might be a bootstrapper who can only afford 2-3X multiple.

The 2025 macro environment (high interest rates) particularly affects strategic buyers. If the buyer needs to finance the deal with corporate debt at 7-8%, they can't justify paying 6X multiples. They'll offer 3-4X instead.

Putting It Together: Real Examples from 2024-2025

Let's look at a few real acquisitions and see how these factors explain the multiples:

Example 1: Predictology (Sports Prediction SaaS)

- Exit Price: $720,000

- Annual Revenue: ~$445K USD

- Multiple: ~1.6X revenue

- Why so low? This was a 10-year-old business with a long track record, but likely slow growth (acquiring a mature, stable business with decades of sports data). The buyer was paying for the database and customer base, not future growth. Still, the long-term stability and competitive moat from the data justified a sale (even at lower multiple) versus letting it decline.

Example 2: Median Cobrowse (Screen Sharing SaaS)

- Exit Price: $280,000

- ARR: $75,000

- Multiple: ~3.7X ARR

- Why this multiple? A modest ARR with a serviceable multiple. The buyer likely saw growth potential (cobrowsing is relevant for modern support teams) but needed the metrics to work with 3.7X financing costs. This suggests a financial buyer rather than a strategic buyer.

Example 3: Userflow (No-Code Onboarding SaaS)

- Exit Price: $60+ million

- ARR: $4.6 million

- Multiple: ~13X ARR

- Why so high? This is a strategic acquisition. Beamer (the buyer) was a feature-adjacent product that could integrate Userflow's capabilities. The 13X multiple reflects synergies unique to Beamer—they can integrate it, sell it to their customer base, and eliminate a competitor. A financial buyer would never pay 13X. Also note: Userflow was bootstrapped with just 3 people, suggesting incredible margins and efficiency. The team and product quality justified the premium.

Example 4: Anonymous Call Tracking SaaS

- ARR: $304,000

- Profit Margin: 89%

- Why this is notable: 89% margins is exceptional for SaaS. This business is probably printing cash. A buyer evaluating this would see strong profitability and low risk. They'd likely offer 4-5X earnings (which might be ~$1.2M-$1.5M acquisition price). Compare this to a comparable $300K ARR company with 40% margins—that might only fetch 2.5-3X earnings.

The Critical Warning: AI-Powered SaaS and Durability Risk

If you're building SaaS on top of OpenAI's API, Claude, or Google's models, you need to read this section carefully. It will directly affect your exit multiple—and possibly whether anyone wants to buy you at all.

The Pattern: Foundation Model Companies Build Your Features

Here's what's happened repeatedly in tech history:

- Email: For decades, standalone email companies (Mailbox, Inbox, etc.) existed as separate products. Then Google integrated Gmail directly into Workspace. The standalone email market collapsed.

- Image Generation: Midjourney, Stability AI, and others built entire companies around generative AI image creation. Then OpenAI integrated DALL-E into ChatGPT. Google integrated Imagen. The standalone image generation market compressed.

- Video Editing: Dozens of companies built AI-powered video editing tools. Then Adobe integrated Firefly into Premiere Pro. The niche AI video editing market is now threatened.

- Code Generation: GitHub Copilot integrated directly into VS Code. Codeium and other standalone code assistants now compete on the margin.

- Writing Assistants: Standalone AI writing tools (Copy.ai, Jasper, etc.) exploded in 2023. Then ChatGPT became free and OpenAI added plugins. The standalone market compressed.

The pattern is clear: when the foundation model company (OpenAI, Google, Anthropic) can integrate a feature directly into their product, they will. And when they do, the standalone SaaS company built on top of that feature becomes significantly less valuable.

Why This Matters for Your Acquisition Multiple

A buyer evaluating a $500K ARR AI writing assistant in 2025 needs to answer a critical question: "How long until OpenAI integrates this directly into ChatGPT?"

If the honest answer is "18-24 months," then your current $500K ARR might evaporate. A savvy buyer will discount your multiple dramatically—or walk away entirely.

Here's the math a buyer does:

- Your current ARR: $500K

- Your expected multiple: 4X earnings (assume 70% margins, so $350K earnings)

- Expected price: $1.4M

- But: If OpenAI integrates your core feature in 18 months, your ARR drops to $100K by month 24 (90% churn as customers move to the free/integrated alternative)

- At that point, your business might only be worth $200K-$300K (valued on cash flow, not multiple)

- The buyer's risk: They're paying $1.4M for something that might be worth $300K in 2 years

- The solution: Buyer offers 1.5X-2X multiple instead, or passes entirely

This isn't hypothetical. Buyers in 2025 are actively applying this discount to AI wrapper valuations.

How to Evaluate Your Own Durability Risk (Honest Assessment)

Before you try to sell an AI-powered SaaS, answer these questions ruthlessly:

1. Is your core value a feature or a business?

Feature-level risk (high durability risk): Your entire product is "AI-powered writing assistance" or "AI image backgrounds." These are features, not businesses. OpenAI or Google will build them in 12-24 months.

Business-level value (lower durability risk): Your product solves a specific workflow problem for a specific customer type. Example: "AI-powered customer support automation for e-commerce brands" with integrations to Shopify, inventory systems, and email platforms. This is harder to commoditize because it's not just the AI—it's the specialized integrations and domain expertise.

Question to ask yourself: If OpenAI released an identical AI engine (same capabilities, same cost), would your customers still use your product? If the answer is "no," you have feature-level risk.

2. Is there a moat beyond the model?

Do you have:

- Domain-specific training data that improves your output for a specific use case? (Lower risk: harder to replicate)

- Integrations with enterprise systems (Salesforce, HubSpot, Workday, etc.) that create lock-in? (Lower risk: switching costs increase)

- Customer relationships and brand loyalty in a vertical? (Medium risk: can be disrupted, but less quickly)

- Proprietary workflows or UX that improve on the base model? (Medium risk: can be copied, but takes time)

If your moat is purely access to the underlying model (you're just wrapping ChatGPT with a UI), you have no defensibility. Your durability risk is high.

3. What's the timeline for the foundation model company to integrate your feature?

Be honest. Not "if," but "when" and "how soon."

- 0-12 months: Feature is likely already on the roadmap. Very high risk. Multiple discount: 60-70%

- 12-24 months: Foundation model company could realistically build this. High risk. Multiple discount: 40-50%

- 24-36 months: Possible but not immediate. Medium risk. Multiple discount: 20-30%

- 3+ years: Would require significant effort or changes to core product. Lower risk. Minimal discount.

Use this framework to estimate your own timeline. Then assume the foundation model company moves faster than you think.

| Timeline to Integration | Risk Level | Multiple Discount | Implications |

|---|---|---|---|

| 0-12 months | 🔴 Critical Risk | -40% | Feature likely already on foundation model roadmap. Buyer assumes rapid commoditization. |

| 12-24 months | 🟠 High Risk | -25% | Foundation model company could realistically build this in 12-24 months. |

| 24-36 months | 🟡 Medium Risk | -15% | Possible but not immediate; requires some product development effort. |

| 3+ years | 🟢 Low Risk | -5% | Would require significant effort or fundamental product changes. Higher defensibility. |

4. Do you have expansion revenue beyond the AI feature?

If your $500K ARR breaks down as:

- $400K from "AI writing assistance"

- $100K from integrations, templates, enterprise support, etc.

Then even if AI writing assistance gets commoditized, you still have a $100K revenue base. That's better than $0K, and it means your multiple discount is less severe.

Buyers like this because it means you have some revenue defensibility beyond the AI layer.

Real Impact on 2025 Multiples

Here's how this plays out in practice:

Scenario 1: Pure AI Wrapper

- Product: AI-powered customer email writing tool

- ARR: $500K

- Expected multiple (without risk): 4X earnings = $1.4M

- Durability assessment: OpenAI could integrate this in 12 months

- Applied discount: 70% (high risk)

- Actual offer: ~$420K (3X ARR, or ~1.2X earnings)

Scenario 2: AI + Vertical Integration

- Product: AI-powered customer support for e-commerce brands (Shopify + inventory + email integration)

- ARR: $500K ($350K AI core, $150K from integrations and enterprise features)

- Expected multiple: 4X earnings = $1.4M

- Durability assessment: OpenAI could build basic AI chat in 12 months, but replicating Shopify/inventory integrations takes longer

- Applied discount: 25% (medium risk)

- Actual offer: ~$1.05M (3X earnings, close to original expectation)

| Metric | Pure AI Wrapper | AI + Vertical Moat |

|---|---|---|

| Product | AI email writing tool | AI support + Shopify + inventory integrations |

| Annual Recurring Revenue | $500K | $500K |

| Expected Earnings Multiple | 4.0X | 4.0X |

| Expected Valuation | $1.4M | $1.4M |

| Durability Risk | 🔴 Critical (12mo) | 🟡 Medium (24-36mo) |

| Applied Discount | -70% | -25% |

| 💰 Actual Offer | $420K | $1.05M |

| Difference | 💡 +150% difference driven entirely by defensibility | |

How to Protect Your Multiple

If you're building AI-powered SaaS and want to maximize your exit multiple, you need to build defensibility:

1. Build domain expertise and data moats

Train custom models or fine-tune base models on domain-specific data that only you have. Make your AI output better for your specific use case than the generic foundation model.

2. Integrate deeply into customer workflows

Don't be a standalone tool. Integrate into your customer's existing systems (Salesforce, Slack, email, etc.). Make switching costs high.

3. Focus on vertical specialization

Instead of "AI for everyone," build "AI for e-commerce customer support" or "AI for legal document review." Make your product indispensable in that vertical.

4. Build beyond the AI layer

Create revenue from services, integrations, enterprise support, custom workflows, and domain expertise. Don't let 80%+ of your revenue come from a single AI feature.

5. Think about your buyer's perspective

Who would actually want to acquire you? If the answer is "only someone in my vertical who wants to eliminate competition," you have limited buyer options. If the answer is "any SaaS company wanting to add this capability," you have strong buyer demand.

The Bottom Line

AI-powered SaaS can be incredibly valuable. But in 2025, buyers are pricing in durability risk. If your entire product is a wrapper around a foundation model's core feature, expect your multiple to be 50-70% below comparable non-AI SaaS.

If you've built defensibility—vertical focus, domain data, integrations, expanding revenue—your multiple can be comparable to traditional SaaS.

Know your durability risk honestly. Price your company accordingly. And if you want to maximize your exit, build defensibility now.

How to Actually Improve Your Acquisition Multiple (Before You Sell)

Now that you understand what drives multiples, the question is: what can you actually do to improve yours?

The answer depends on your timeline. If you're planning to exit in 3 months, your options are limited. If you have 12-24 months, you have real levers to pull.

The Levers, Ranked by Impact

Lever 1: Improve Your Growth Rate (Biggest Impact)

This is the single biggest driver of multiples. A company growing at 30% YoY can command 1.5-2X higher multiples than a company growing at 10% YoY, all else equal.

But here's the problem: Growing faster takes work, time, and usually money. You can't just flip a switch.

Realistic growth initiatives (6-12 month timeline):

- Improve product-market fit: Talk to your customers. Why do they churn? What features would make them expand? Build those things. Even a 5-10% improvement in retention can compound into 15-20% revenue growth over a year.

- Expand into adjacent use cases: If you're a customer support tool, can you become a customer data platform? If you're email marketing, can you do SMS? New use cases drive new customer segments and higher growth.

- Increase pricing: Not growth in customers, but growth in revenue per customer. A 20% pricing increase (with minimal churn) directly increases your ARR and your multiple. Works especially well if you have strong net retention (expansion revenue).

- Focus sales on high-LTV customers: Instead of chasing volume, focus on landing bigger customers with higher LTV. This improves customer concentration (more valuable customers) and often improves margins (bigger deals have better unit economics).

- Launch new features for existing customers: Build things that existing customers will pay more for. This improves NRR, which directly improves your multiple.

Impact on multiple: Moving from 10% to 25% YoY growth can increase your multiple by 0.5-1X (depending on margins and risk). That's a 15-25% improvement in exit value.

Lever 2: Improve Unit Economics and Profitability

This is faster to execute than growth, and it has a big impact on multiples.

Key metrics to improve:

- Gross Margin: Every 10% improvement in gross margin can improve your multiple by 10-15% (assuming the same ARR). Lower COGS = more cash, higher profitability.

- Churn Rate: Reducing monthly churn from 5% to 3% is huge. Monthly churn is the inverse of retention. At 5% monthly churn, your customers are worth less because they leave quickly. At 3%, they're more valuable.

- Net Retention Rate (NRR): If you can improve from 95% NRR (slight churn) to 105% NRR (expansion revenue), that's a 10 percentage point improvement that directly justifies higher multiples.

- CAC Payback Period: Reduce the time it takes to recoup customer acquisition costs. This improves cash flow efficiency and shows buyers a more efficient business.

- Profitability: If you're currently losing money, becoming EBITDA-positive is a game-changer. EBITDA-positive SaaS commands 1.5-2X higher multiples than pre-profitability companies.

Quick wins (3-6 months):

- Reduce churn: Audit why customers are leaving. Fix the top 2-3 reasons. Can you reduce churn by 1-2 percentage points? That's worth 5-10% higher multiple.

- Improve pricing: A 15-25% price increase for new customers (keep existing customers grandfathered) improves gross margins and revenue without increasing costs. Tests can happen in 4-6 weeks.

- Cut unnecessary costs: Do you have tools or contractors you don't actually need? Cut them. Improve your profit margin.

- Upsell to existing customers: Build one upsell offering (higher tier, add-on feature, premium support). Even 10% of customers upgrading adds 10%+ to NRR.

Impact on multiple: Moving from -10% EBITDA margin to +20% EBITDA margin can increase your multiple by 0.75-1.5X. That's a 20-40% improvement in exit value.

Lever 3: Reduce Customer Concentration Risk

If your top customer is 20% of revenue, buyers get nervous. If you can reduce that to 8%, your multiple improves immediately.

How to reduce concentration:

- Land more customers: Obvious, but if you can double your customer count in 12 months without losing your top customer, concentration drops by ~50%.

- Diversify your customer base: If 40% of your revenue is from one industry, focus on landing customers in 3-4 other industries. Industry diversification also reduces risk.

- Build self-serve to replace big deals: If you're currently 70% enterprise (2-3 big customers) and 30% SMB, shift the mix. More smaller customers = lower concentration.

Impact on multiple: Reducing customer concentration from 25% single-customer to 8% can improve your multiple by 15-25% (on the same ARR). Buyers will pay more for a less risky business.

Lever 4: Clean Up Technical Debt

This is often overlooked, but a buyer will discount your multiple 20-50% if your codebase is a mess.

What buyers check:

- Do you have automated tests? (Missing tests = -20% discount)

- Is the codebase documented? (No docs = -10% discount)

- Is it on a modern tech stack? (5+ year old framework = -10% discount)

- Can new engineers understand the code quickly? (Complex/undocumented = -20% discount)

- Are there obvious bugs or technical issues? (Yes = -30% discount)

Quick improvements (6-12 months):

- Add test coverage to critical paths (don't test everything, just core features and payment/auth systems)

- Write a 1-page architecture document and API documentation

- Fix the top 5-10 technical issues that cause support tickets

- Upgrade major dependencies to current versions (so the buyer doesn't inherit tech debt immediately)

Impact on multiple: Addressing major tech debt can improve your multiple by 15-30%. A buyer paying less to fix your mess is less likely to discount your price.

Lever 5: Build Deal Structure Optionality

You can't control what offer you'll get, but you can control what structures you're willing to accept. This affects your effective multiple.

Before you start talking to buyers, decide:

- What's your minimum cash-at-close requirement? (Do you need all cash now, or are you OK with 50% at close + 50% earnout if the multiple is higher?)

- Will you consider seller financing? (At what discount to headline multiple?)

- Would you stay post-acquisition? (If yes, you can negotiate earnout targets that you believe in)

- What level of earnout contingency are you comfortable with? (10%? 30%? 50%?)

Having clear answers to these questions means you can negotiate effectively. You might accept a 3.8X headline multiple with all cash if you wouldn't accept 4.5X with 50% earnout risk.

Impact on multiple: By being flexible on structure, you can often achieve an effective multiple 0.3-0.5X higher than a founder who only wants "all cash, no earnout." That's worth 5-15% on your final valuation.

Lever 6: Build Defensibility and Durability (Especially for AI SaaS)

If you're AI-powered, this matters enormously. If you're not, it still matters.

Durability moats to build:

- Domain-specific data or models: Train a custom model on domain-specific data (legal documents, medical records, customer support conversations). This makes your AI better for your specific use case.

- Integrations: Integrate with 3-5 tools your customers use (Salesforce, Slack, email, etc.). Switching costs increase.

- Vertical specialization: Instead of "AI for everyone," own "AI for e-commerce customer support." Build product and marketing specifically for that vertical. Defensibility improves.

- Expand beyond the AI feature: Build complementary revenue streams (services, training, premium support). Reduce dependence on the AI feature alone.

Impact on multiple: For AI SaaS, building defensibility can increase your multiple by 1-2X. Without it, expect a 50-70% discount to non-AI comparable companies.

Timeline: What to Focus On When

| Improvement Lever | Impact | 3 mo | 6-12 mo | 12-24 mo |

|---|---|---|---|---|

| Growth Rate | ⭐⭐⭐ | — | ⚡ | 🎯 TOP |

| Profitability & Unit Econ | ⭐⭐⭐ | 🎯 TOP | 🎯 TOP | ⚡ |

| Defensibility/Durability | ⭐⭐⭐ | — | ⚡ | 🎯 TOP |

| Deal Structure Strategy | ⭐⭐ | ⚡ | ⚡ | ⚡ |

| Tech Debt Cleanup | ⭐⭐ | ⚡ | ⚡ | ⚡ |

| Customer Concentration | ⭐⭐ | — | ⚡ | ⚡ |

Legend: 🎯 TOP = Highest priority | ⚡ = Worth doing | — = Too late to move needle | ⭐ = Relative impact on multiple

If You Have 3 Months

You're already exiting. Focus on:

- Profitability: Cut unnecessary costs. Maximize profit margin. (Improves multiple 15-25%)

- Tech debt: Fix the most obvious issues. (Prevents discount, improves 10-15%)

- Customer concentration: Run the numbers clearly for buyers. Diversify if you can in 2-3 months. (Prevents discount)

If You Have 6-12 Months

You have time to execute. Focus on:

- Profitability and unit economics: Primary focus. Improve NRR, reduce churn, improve margins. (20-40% improvement)

- Growth initiatives: Secondary focus. Try 2-3 growth levers. (10-20% improvement)

- Tech debt: Tertiary focus. Clean up critical issues. (10-15% improvement)

If You Have 12-24 Months

You have time to execute everything. Focus on:

- Growth rate: Primary focus. This has the biggest impact. (15-30% improvement)

- Unit economics: Secondary focus. Improve defensibility and margins. (20-40% improvement)

- Defensibility and moats: Tertiary focus. Build defensibility against competition and foundation model commoditization. (1-2X improvement for AI SaaS)

Realistic Expectations: The Multiple Improvement Potential

If you execute well across these levers over 12 months, how much can your multiple improve?

- Conservative execution (1-2 levers): 15-25% improvement

- Solid execution (3-4 levers): 30-50% improvement

- Aggressive execution (all levers): 50-100%+ improvement

A company moving from 3X earnings multiple to 5X earnings multiple (a 67% improvement) would be doing very well. This is achievable if you improve growth rate significantly and improve unit economics substantially.

The key: These improvements compound. A company that grows faster, has better margins, lower churn, and less customer concentration isn't just incrementally more valuable—it's exponentially more valuable to a buyer.

What Multiples Mean for You: It Depends on Your Situation

Here's something most articles about SaaS multiples miss: the same multiple means completely different things depending on your situation.

A 4X earnings multiple is fantastic for a bootstrapped founder. It's disappointing for a venture-backed founder. It's unachievable for a pre-revenue startup. Context matters.

For Bootstrapped/Profitable Founders

If you built your SaaS without raising money and it's profitable, multiples work differently for you.

What you care about: Total cash in the bank post-exit, and how quickly you get it.

Healthy multiple range for you: 3-5X earnings (for stable, slow-growing businesses) or 4-6X earnings (for faster-growing, profitable businesses)

Why? Because you don't have investor expectations to meet. You don't need a 10X exit to make your returns work. A 4X exit on a profitable business is legitimately great. It means you built something valuable that someone is willing to pay substantial cash for.

Real example: Zencast sold for 3.48X earnings on an all-cash basis. For a bootstrapped founder, this is a successful exit. You got cash, certainty, and the deal closed fast. You're done.

Your decision framework:

- Do you have a specific number you need to hit (financially)? If yes, work backward from that number to calculate the multiple you need.

- Are you comfortable with earnouts, or do you want all cash now? (All-cash might mean accepting a lower headline multiple, but you get certainty.)

- Would you want to stay post-acquisition? (If yes, you can negotiate earnout terms you believe in, and accept a higher headline multiple with lower upfront cash.)

For Venture-Backed Founders

If you raised money (seed, Series A, Series B), multiples work very differently.

What you care about: Making your investors' returns work, and how that translates to your equity value.

What investors expect:

- Seed investors: Typically expect 5-10X returns (so a $1M seed wants the company to be worth $5M-$10M at exit). A 4X earnings multiple might be acceptable if your ARR is high enough.

- Series A investors: Typically expect 3-5X returns from Series A forward (so a $5M Series A wants the company to be worth $15M-$25M+ at exit). A 3X earnings multiple might be insufficient.

- Series B+ investors: Increasingly expect exits at $100M+ valuation. Multiples matter less; absolute exit value matters more.

The multiple that matters for you: Not the acquisition multiple directly, but the multiple on investor capital. If Series A invested at a $15M valuation and you exit at $50M, that's a 3.3X return on Series A. That's acceptable, not great.

Real example: Imagine you have $10M ARR, raised a $5M Series A at a $25M post-money valuation, and get an offer at 4X earnings ($40M valuation). Series A wants to know: "How much of that $40M is going to LP returns vs. management and employee options?" If Series A has 20% equity, they get $8M. They invested $5M, so 1.6X return. That's disappointing.

For venture-backed founders: Multiples are secondary. Total exit value is what matters. You might prefer a lower multiple on a larger base ($3M ARR at 5X = $15M) over a higher multiple on a smaller base ($1M ARR at 6X = $6M).

Your decision framework:

- Calculate the exit value your investors need to hit their return targets. Work backward from that.

- Be realistic about whether that exit value is achievable. If not, you have a problem that no multiple can fix.

- Focus on growing your ARR, not chasing a specific multiple. A higher base with a lower multiple often beats a lower base with a higher multiple.

For Pre-Revenue / Early-Stage Founders

If you're pre-revenue or very early revenue, acquisition multiples don't apply to you in the traditional sense.

How you get valued instead:

- Talent acquisition (acquihire): Buyer is paying primarily for the team, not the business. $500K-$2M depending on team quality and buyer size.

- Technology acquisition: Buyer is paying for your IP, tech, or strategic positioning. Often $1M-$5M depending on how unique your tech is and how valuable it is to the buyer.

- Growth potential acquisition: Buyer believes in your vision and market, and is paying for growth potential. Highly variable, $2M-$20M depending on the market size and buyer conviction.

In these cases, multiples are meaningless. You're not valued on revenue or earnings—you're valued on potential and strategic fit.

For Different Buyer Types

The buyer's identity also changes what multiples mean.

Strategic Buyer (Larger Company in Your Space)

What they care about: Strategic value (eliminating competition, adding customers, adding features, expanding market presence)

Multiple range: 5-8X earnings (higher than financial buyers because of synergies)

What this means for you: Strategic buyers will pay more, but they'll also integrate your product, team, and customers differently. You might lose autonomy, but the valuation is often better.

Example: Userflow (the $60M acquisition) was bought by Beamer, a strategic buyer who could integrate the product and sell it to their customer base. Financial buyer might have offered $20-30M. Beamer offered $60M+ because the synergies were valuable.

Financial Buyer / PE Firm

What they care about: ROI on the investment (typically 20-30% IRR)

Multiple range: 3-5X earnings (conservative; needs to work financially)

What this means for you: PE firms are disciplined about multiples. They won't overpay. But they're also reliable—they'll close. And they often want the founder/management team to stay on (which might or might not be appealing).

Individual Buyer / Competitor

What they care about: Variable. Might be a competitor wanting to eliminate you. Might be an individual wanting to scale your business. Might be someone who just loves the idea.

Multiple range: 2-6X earnings (high variability)

What this means for you: Highly unpredictable. Could be great, could be terrible. More room for negotiation, but also more risk of the deal falling through or terms changing.

Decision Framework: Should You Take This Offer?

When you get an acquisition offer, here's how to evaluate whether it's good:

Step 1: Calculate your "walk-away" number

How much cash do you need? Account for:

- Personal financial goals (what do you want to be paid?)

- Reinvestment (will you start another company? How much capital do you need?)

- Taxes (exit at $2M, you owe taxes on gains. Net might be $1.5M.)

- Investor returns (if you raised money, calculate what your equity stake is worth and ensure it meets your expectations)

Once you have this number, ignore the headline multiple. Does the offer get you to your number? Yes = serious consideration. No = pass or counter.

Step 2: Evaluate deal structure

The headline multiple matters less than the structure. Evaluate:

- Cash at close vs. contingent payments (earnout, seller financing, etc.)

- Earn-out risk (can you hit the targets? Will the buyer move goalposts?)

- Your involvement post-close (do you want to stay? Can you leave?)

Step 3: Compare to the alternative

What's your alternative? Continue running the company? Raise more money? The offer should be better than your best alternative.

Step 4: Get professional help

This is the most important financial decision you'll make. Hire a lawyer and accountant experienced in SaaS M&A. Their fee ($5K-$15K) is worth it.

The $500M Inflection Point: Why Size Changes Everything

One of the most important insights you need to understand: acquisition multiples and valuation mechanics change dramatically based on company size.

There isn't one "right" multiple for SaaS. There are different multiples for different market segments, and the rules change at certain inflection points.

Note: Earnings multiples for smaller sizes, revenue multiples for larger sizes. $500M+ ranges are highly buyer-dependent.

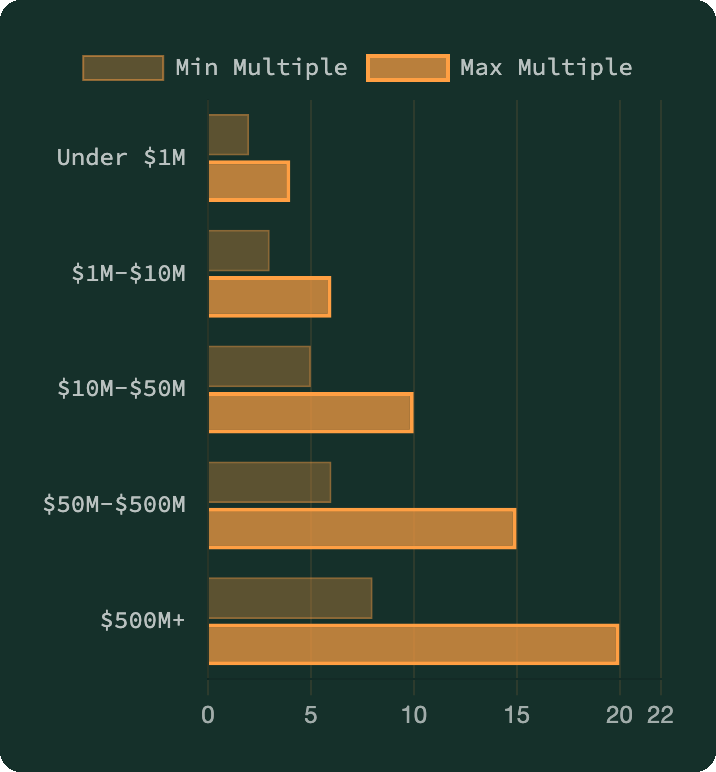

Micro-SaaS: Under $1M ARR

Valuation model: Earnings-based or SDE (Seller Discretionary Earnings)

Multiple range: 2-4X earnings

Who buys: Individual buyers, small agencies, small PE firms, sometimes larger SaaS companies looking for tuck-ins

What matters:

- Profitability and cash generation (are you EBITDA positive?)

- Churn (how stable is the revenue?)

- Customer concentration (is it concentrated? Risky.)

Why lower multiples? Micro-SaaS businesses are smaller, often have higher churn, limited management, and operational risk. A buyer can't implement sophisticated financial engineering. The business needs to work on fundamentals.

Example: Median Cobrowse sold for 3.7X ARR. This is typical for a bootstrapped micro-SaaS with modest but stable revenue.

Small SaaS: $1M-$10M ARR

Valuation model: Revenue-based or earnings-based (hybrid)

Multiple range: 3-5X revenue / 3-6X earnings

Who buys: Mid-market PE firms, larger SaaS companies, strategic acquirers, occasionally venture-backed companies in the space

What matters:

- Growth rate (are you accelerating or decelerating?)

- Unit economics (NRR, churn, CAC payback)

- Profitability trajectory (are you on path to profitability?)

- Management team (can the buyer keep the business running with existing management?)

Why this range? Companies at this size are big enough to show real traction and sustainable models, but small enough that a single buyer can integrate and optimize them. Multiples reflect this—better than micro-SaaS, but not yet in the "proven large company" range.

Example: Castanet and Zencast both fit in this range and exited at 3-3.5X earnings multiples.

Mid-Market SaaS: $10M-$50M ARR

Valuation model: Revenue-based (primary) or earnings-based (if profitable)

Multiple range: 4-8X revenue / 5-10X earnings

Who buys: Large PE firms, strategic acquirers (other SaaS companies), venture-backed companies, occasionally public companies

What matters:

- Growth trajectory (are you 30%+ YoY? 50%+? That justifies higher multiples)

- Market position (are you a leader in your segment?)

- Management depth (do you have a real management team, or is it all founder-driven?)

- Customer base quality (are customers sticky? High ACV?)

Why higher multiples? At $10M+ ARR, you've proven product-market fit, have sophisticated operations, and represent a meaningful business. Buyers can finance these acquisitions with debt, and the math works. There are also more potential buyers (more strategic acquirers at this size).

Example: Userflow likely exited for ~13X revenue, but that's a strategic acquisition (Beamer buying a feature-adjacent product for integration purposes). A financial buyer might have paid 5-7X revenue on the same metrics.

Large SaaS: $50M-$500M ARR

Valuation model: Revenue-based (primary) with strategic premium adjustments

Multiple range: 6-15X revenue (highly variable based on growth and buyer)

Who buys: Large strategic acquirers (enterprise software, cloud platforms, Fortune 500), PE mega-funds, occasionally public companies

What matters:

- Growth rate (30%+ YoY growth? 50%+?)

- Market category (are you in a hot market or a slow market?)

- Strategic fit (how valuable is this to potential acquirers?)

- Customer composition (do you have Fortune 500 customers? That's worth a premium.)

- Financial performance and track record (have you been consistently profitable or growing?)

Why such a wide range? At this size, the buyer list is more selective, so "strategic value" becomes heavily weighted. A vertical SaaS owning a market niche might command 12X revenue. A horizontal SaaS in a crowded market might only get 6X revenue. The difference is strategic fit, not just growth rate.

Mega-SaaS: $500M+ ARR (The Inflection Point)

This is where everything changes.

Valuation model: Still revenue-based, but heavily customized to the buyer

Multiple range: 8-20X+ revenue (but this number is almost meaningless)

Who buys: Almost exclusively strategic (Salesforce, Microsoft, Google, Oracle, Adobe, etc.)

Critical insight: At $500M+ ARR, multiples are no longer based on a spreadsheet calculation that works for "any buyer." The valuation is almost entirely strategic—unique to each potential acquirer based on the specific synergies only they can extract.

Why? Because:

- Financing changes: A $5B acquisition isn't financed with typical debt anymore. It's a strategic fit that justifies the price within a large acquirer's portfolio.

- Synergy value is enormous: Salesforce buying a $500M ARR company isn't paying for the company's standalone cash flows. They're paying for customer overlap, cross-selling opportunities, product integration, market presence, and talent. Synergies could be worth $2B+ to Salesforce but $0 to a financial buyer.

- The multiple depends entirely on the buyer: Company A might pay 15X revenue because they see $2B in synergies. Company B might pay 8X revenue because they see $500M in synergies. A financial buyer might walk away because they can't justify any multiple (they need to work on fundamentals, not synergies).

- The spreadsheet doesn't close the deal: At this scale, the buyer's CFO isn't saying "15X revenue is too high." They're saying "our internal models show $2B in synergies, so paying $7B is worth it." The multiple is downstream of strategic value, not the primary constraint.

Real example: When Microsoft acquired LinkedIn for $26.2B on ~$600M ARR (43X revenue), investors screamed "that's insane!" But for Microsoft:

- LinkedIn customers (professional users) could be introduced to Microsoft products (Azure, Office 365, Teams)

- Microsoft's customer base (businesses) could use LinkedIn for recruitment and talent management

- Data integration with Microsoft's enterprise products was enormous value

- The synergies were worth far more than 43X revenue—potentially $5B+ annually in new revenue or cost savings

A financial buyer couldn't have made that math work. A strategic buyer (Microsoft) could make it work easily.

The Implication for You

Understanding size stratification matters because:

If you're building toward a $2M-$10M ARR exit: Focus on the factors we discussed—growth, profitability, unit economics, and deal structure. Multiples in the 3-5X range are realistic, and you can influence your multiple significantly.

If you're building toward a $50M+ ARR exit: Growth rate becomes more important, but so does market category and strategic fit. You need to build in a hot market or own a defensible vertical to justify higher multiples.

If you're building toward a $500M+ ARR exit: You're not really targeting a specific multiple. You're positioning yourself to be strategically valuable to one of 5-10 potential acquirers. The multiple will be whatever that acquirer values the synergies at. Your job is to pick the right category, build a defensible position, and make yourself attractive to potential strategics.

The Bottom Line on Size

Don't optimize for a multiple. Optimize for:

- If you're $1M-$10M: Profitability, unit economics, and defensibility. Multiples will follow.

- If you're $10M-$100M: Growth rate and market position. Multiples will follow.

- If you're $100M+: Strategic positioning and dominance in your category. Multiples (and absolute valuation) will follow.

Future Outlook: When Will Multiples Recover?

The question every founder asks: "Are we at the bottom? When will multiples recover to 2021 levels?"

The honest answer: Not for a while. And it has nothing to do with how good your product is.

The Macro Headwind: Why Multiples Are Structurally Compressed

Recall from earlier: acquisition multiples are directly downstream of the buyer's cost of capital. When debt is expensive, multiples compress. When debt is cheap, multiples expand.

The current problem: The U.S. federal government is running massive budget deficits. The political environment is primed to "solve" this through inflation rather than fiscal austerity (cutting spending or raising taxes). When inflation is high, the Federal Reserve raises interest rates to combat it. And when interest rates are high, debt is expensive, and acquisition multiples compress.

This creates a structural headwind that's independent of how well any individual SaaS company performs.

The timeline for potential improvement:

- 2025: Interest rates likely remain elevated. Expect current multiple ranges (3-5X for stable SaaS, 4-6X for growth). No meaningful recovery.

- 2026: Possible modest improvement if inflation trends cool. Might see 3-6X for stable, 5-7X for growth. Still below 2021 peaks.

- 2027+: Meaningful recovery possible only if the Fed significantly lowers rates and holds them there. This requires either inflation to truly subside, or political will to address deficits. Neither is certain.

Scenario Analysis: Three Potential Futures

Scenario 1: Rates Stay High (Base Case, 60% Probability)

Interest rates remain elevated (6-8% for corporate debt) for the foreseeable future because inflation remains sticky and the Fed won't cut significantly.

Multiple outlook: Current ranges hold. 3-5X for stable, 4-6X for growth. No meaningful improvement until 2028+.

What to do: Don't wait for multiples to recover. Build and exit on fundamentals. A 4X multiple on a profitable, growing business is a legitimate exit in this environment.

Scenario 2: Inflation Cools, Rates Drop (Upside Case, 25% Probability)

Inflation trends subside, the Fed cuts rates materially, and we move into a lower-rate environment by 2026-2027.

Multiple outlook: Multiples expand by 20-40%. 3-6X for stable becomes 4-8X. 4-6X for growth becomes 5-9X. Still below 2021 peaks, but meaningful improvement.

What to do: If you can hold 18-24 more months, the upside is real. But don't count on it. Lock in gains when they're available.

Scenario 3: Stagflation or Economic Shock (Downside Case, 15% Probability)

Inflation persists, growth slows, the economy enters a recession, and rates stay high or go higher to fight inflation.

Multiple outlook: Multiples compress further. 2-3X for stable, 3-4X for growth. Buyers retreat to only the most profitable, defensible businesses.

What to do: Ensure profitability and strong unit economics now. In a downside scenario, only truly healthy businesses attract buyers.

What This Means for Your Exit Timeline

If you can exit in the next 6-12 months: Current multiples (3-5X) are realistic and locked in. Don't wait for a potential recovery.

If you're planning 12-24 months out: You have optionality. You can either exit now at current multiples, or hold for potential upside if rates drop. Build defensibility so you're attractive in either scenario.

If you're planning 2+ years out: Rates might improve. But don't count on it. Focus on building a business that's valuable regardless of macro conditions. Profitable, defensible, growing. Those fundamentals work in any interest rate environment.

What's Actually Changing in the SaaS M&A Market

Beyond macroeconomic headwinds, the SaaS acquisition market is also shifting in a few structural ways:

1. Buyers are more selective

Strategic acquirers are more cautious about overpaying. They're evaluating ROI tightly. This pushes multiples down even for good companies.

2. Earnouts are becoming more common

Buyers want less upfront risk. Expect more deals to include 30-50% earnout components. This reduces effective multiples for founders.

3. PE is more disciplined

PE firms have tightened their underwriting. They need deals to work on fundamentals, not hope for operational improvements post-close.

4. AI SaaS valuations are being repriced

As we discussed, AI wrapper companies are seeing 30-70% discounts due to durability concerns. This is new and structural.

5. Profitable SaaS is more valued than ever

Paradoxically, while growth-at-all-costs is out, profitable SaaS is commanding premiums. EBITDA-positive businesses see higher multiples relative to revenue than pre-profitability companies.

The Founder Playbook for 2025-2026

If you want to maximize your exit value in this environment:

- Prioritize profitability. EBITDA-positive SaaS is more valuable than pre-profitability SaaS at the same growth rate. This is different from 2021.

- Focus on defensibility and durability. In uncertain macro conditions, buyers pay premiums for companies they're confident will still be around in 3 years.

- Build multiple revenue streams. Don't depend on a single feature or customer. Diversification justifies higher multiples.

- Reduce customer concentration. In a recession scenario, concentration risk is heavily penalized.

- Be flexible on deal structure. You might get a lower headline multiple if you accept earnout risk or seller financing. Calculate your effective value.

- Don't wait for multiples to recover. Current multiples are sustainable and realistic. Waiting for 2021 peaks to return is wishful thinking.

AI SaaS Deal Structure: Terms That Matter More Than Headline Multiple

For traditional SaaS, founders fixate on multiple and cash at close. For AI SaaS, that is incomplete. If model risk or margin volatility is high, the deal can look great at signing and underperform badly 6-12 months later. The right structure protects both sides.

In 2026, most serious AI SaaS buyers are underwriting three risks explicitly: retention durability, inference margin compression, and provider dependency. If your term sheet does not clearly allocate those risks, you should expect painful renegotiation in diligence.

| Term | Buyer-Protective Baseline | Founder-Fair Compromise |

|---|---|---|

| Earnout Metric | Retention + gross margin gates, measured monthly for 12 months. | Use blended targets with a cure period and explicit exclusions for buyer-caused disruptions. |

| Model Provider Risk | Specific adjustment rights if core provider reprices or deprecates APIs. | Time-boxed repricing clauses and shared migration responsibility. |

| Data/IP Reps & Warranties | Full representation of data rights, consent flows, and provider TOS compliance. | Defined materiality thresholds and capped survival periods for lower-risk items. |

| Transition Services | 90-day mandatory founder transition for model tuning, prompt architecture, and eval transfer. | 60 days mandatory + optional paid extension with predefined rates and scope. |

| Quality Regression Trigger | Earnout protection if quality metrics degrade materially post-close. | Use shared eval benchmarks and jointly controlled test sets agreed pre-close. |

Practical guidance: tie contingent consideration to metrics both parties can verify and influence. Avoid vague terms like "continued model performance" without benchmark definitions. If metrics are ambiguous, disputes are almost guaranteed.

Also build a post-close 30/60/90 integration plan into the purchase process: model fallback setup, prompt and eval migration, support workflow updates, and pricing/packaging adjustments for inference cost stability. Deals close faster when this plan exists before legal docs are final.

If you are evaluating targets, pair this section with our AI SaaS due diligence checklist. If you are structuring or negotiating a deal, use the full AI SaaS acquisition playbook. If you are choosing buyers, use the AI seller checklist to pressure-test acquirer fit before signing exclusivity.

The Bottom Line: SaaS Acquisition Multiples in 2025

Let's recap the key frameworks you need to understand SaaS acquisition multiples:

What Determines Your Multiple

- Growth rate: The single biggest driver. 30% growth justifies higher multiples than 10% growth.

- Unit economics: Profitability, churn, NRR, and margins matter more than raw revenue.

- Durability: Especially critical for AI SaaS. Can the foundation model company build your feature in 18 months? If yes, discount your multiple 30-70%.

- Deal structure: All-cash might mean a lower headline multiple but zero risk. Earnouts might mean higher multiples but higher risk. Calculate effective value, not headline multiple.

- Macro conditions: High interest rates compress multiples. This is structural, not a reflection of your company's quality.

- Company size: Micro-SaaS gets 2-4X. Mid-market gets 4-8X. Above $500M, it's all strategic value.

The 2025 Multiple Ranges (Quick Reference)

These ranges assume reasonable unit economics (positive or clear path to profitability), low customer concentration (<10% from one customer), and manageable tech debt. Adjust downward 10-30% for each risk factor present in your business.

The Levers You Control

You can't control macro conditions or the buyer's interest rates. But you can control:

- Growth rate (improve via product, marketing, or pricing)

- Unit economics (improve via NRR, churn, and cost structure)

- Customer concentration (land more customers, diversify)

- Tech debt (clean it up)

- Durability (especially if AI-powered)

- Deal structure optionality (decide your preferences pre-offer)

Focus on these. They directly impact your multiple and exit value.

Final Advice

For bootstrapped founders: A 3-4X earnings multiple on a profitable SaaS is excellent. Don't chase 6X multiples. Lock in solid returns.

For venture-backed founders: Forget the multiple. Focus on absolute exit value and whether it meets your investors' return targets. A 3X multiple on $50M ARR ($150M exit) beats a 5X multiple on $10M ARR ($50M exit).

For AI SaaS founders: Durability is your biggest lever. Build defensibility aggressively. The market is repricing AI wrappers harshly, and for good reason.

For all founders: Multiples won't recover to 2021 levels soon. Plan your exit on 2025 fundamentals, not 2021 hopes. The businesses that survive and thrive in this environment are those built on defensible, profitable models—not on momentum and growth-at-all-costs.

Build something real. Build something defensible. Build something profitable. The multiple will follow.

Next Steps

Want actionable frameworks to evaluate your specific situation? Use this process:

- Calculate your current ARR, growth rate, and EBITDA margin

- Identify your biggest "multiple risk" (concentration? Churn? Tech debt?)

- Work backward: What exit value do you need? Divide by your likely multiple to see what ARR you need to hit.

- Build a 12-month plan to improve that specific metric

Ready to connect with founders and SaaS operators in a similar position?

Join the Wildfront Community

Connect with other SaaS founders, operators, and investors who are navigating exits, valuations, and growth strategies in real-time. Share experiences, ask questions, and learn from peers who've been in your shoes.

Or, get monthly SaaS M&A insights delivered to your inbox:

Subscribe to Our Newsletter

Monthly updates on SaaS valuation trends, recent acquisition data, and founder playbooks. No spam, just actionable insights.

Sources & Further Reading

- How to Buy a SaaS Business - Complete acquisition guide from the buyer's perspective: due diligence, deal structuring, and risk mitigation

- Flippa - Real SaaS acquisition data and marketplace

- FE International - SaaS M&A advisory and valuation benchmarks

- Climb Partners - SaaS M&A and operator insights

- Noosa Labs - SaaS metrics and analytics

- Acquire.com - SaaS acquisition marketplace with valuation data

About the author: Alex Boyd is the founder of Wildfront and operator/investor in multiple SaaS businesses. He's exited two SaaS companies (Zencast and Castanet) and works with founders on valuation, M&A strategy, and growth. You can find him on Wildfront.

Join a room of bootstrapped SaaS founders

Wildfront+ is an invite-only mastermind of vetted founders — professionally facilitated calls, honest feedback, no fluff. Or start free with the bootstrapper academy.