Banking guide

Best Business Bank Accounts for Startups for 2026

Compare the best business bank accounts for startups. $250-500 bonuses, venture debt, zero fees. Built for founders who understand burn rate.

![]() By Alex Boyd

By Alex Boyd

You just closed your seed round. Congrats. Now you need a business bank that understands runway, not revenue—because Chase is going to take one look at your negative cash flow and reject your application.

Traditional banks don't work for startups. They want two years of profitability, personal guarantees, and they'll still charge you $25/month for the privilege. Meanwhile, Mercury, Brex, and Rho will approve you based on your funding round, give you credit lines up to 40% of your ARR without a personal guarantee, and pay you $250-500 just to open an account.

The best business banks for startups aren't banks at all—they're fintech companies built by founders who understand burn rate, runway extension, and why you need $100k credit limits before you have revenue. This guide covers everything: from Mercury's investor reporting tools to Brex's venture debt options to Rho's $500 sign-up bonus.

Quick reality check: If you're VC-backed or raising capital, this guide is for you. If you're running a general LLC or service business, check out our LLC banking guide instead.

Quick Comparison: Best Business Bank Accounts for Startups

| Bank | Monthly Fee | Sign-Up Bonus | Venture Debt | Setup Time |

|---|---|---|---|---|

Mercury

Mercury

|

$0 | $250 | Yes | 10 min |

Brex

Brex

|

$0 | Points | Up to 40% ARR | 1 day |

Rho

Rho

|

$0 | $500 | Yes | 1-2 days |

Ramp

Ramp

|

$0 | $250 | Yes | 15 min |

Relay

Relay

|

$0 | None | Limited | 10 min |

What to Look for in a Startup Business Bank Account

Startup-Friendly Underwriting

Here's the fundamental problem: traditional banks underwrite on profitability. Startups are intentionally unprofitable—you're burning capital to acquire customers and build product. That's not a bug, it's the entire business model.

Traditional bank requirements: 2+ years of revenue history, demonstrated profitability, personal credit score 680+, personal guarantee on all credit, collateral or cash deposits.

Startup bank requirements: Proof of funding (term sheet, cap table, or SAFE notes), company formation documents, EIN, government ID. That's it.

Mercury approved our account in 8 minutes with $0 revenue and a $750k pre-seed round. Chase wanted tax returns from a business that was 3 weeks old. The difference matters.

Venture Debt & Non-Dilutive Capital

The best startup banks offer credit lines based on your funding, not your revenue. This is fundamentally different from traditional business credit.

Watch out for:

| Fee Type | Why It Matters |

|---|---|

| Monthly maintenance fees | $15-40/month for basic checking features |

| Transaction limits | Caps at 50-100 transactions/month |

| Wire transfer fees | Charges on incoming and outgoing wires |

| Cash deposit fees | Costly for cash-heavy businesses |

| Minimum balance requirements | Forces idle cash to avoid fees |

The banks we recommend below charge $0/month with no minimums. Traditional banks can't compete.

Setup Requirements & Speed

Opening a business bank account for your LLC requires:

| Document | Notes |

|---|---|

| EIN | Employer Identification Number from the IRS |

| Articles of Organization | Your LLC formation documents |

| Operating Agreement | Some banks require this |

| Government-issued ID | Driver's license or passport |

Fintech banks approve accounts in minutes. Traditional banks take 1-2 weeks and often require in-person visits.

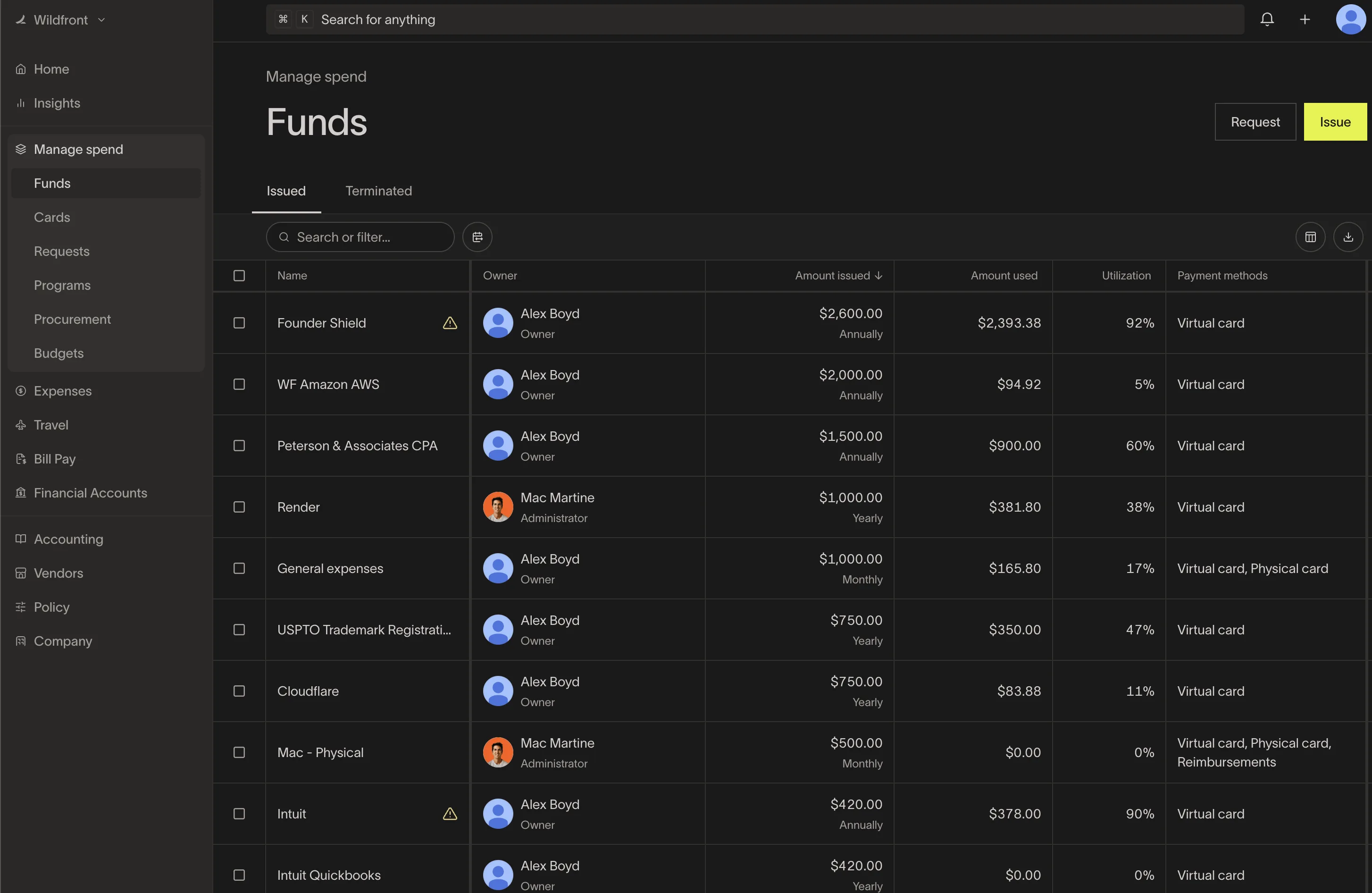

Modern Features That Actually Matter

Your business bank should integrate with your workflow, not create extra work.

Critical integrations:

| Integration Type | Why It Matters |

|---|---|

| Payment processors | Accept payments via Stripe, Square, PayPal |

| Accounting software | Auto-sync books in QuickBooks, Xero, FreshBooks |

| Payroll providers | Run payroll via Gusto, Justworks, Rippling |

| Expense management tools | Manage cards, approvals, receipts |

Useful features:

| Feature | Why It Helps |

|---|---|

| Multi-user access | Set permissions for teammates |

| Virtual debit cards | Create unlimited cards for different expenses |

| API access | Automate workflows and reporting |

| Expense categorization | Reduce manual bookkeeping |

| Invoice management | Track payables in one place |

| Mobile check deposit | Deposit paper checks in-app (available for eligible accounts across Mercury, Brex, Ramp, Rho, Relay, and Novo) |

Cash Back & Sign-Up Bonuses

This is where fintech banks really shine. Instead of charging you fees, they pay you:

| Bank | Sign-Up Bonus | Notes |

|---|---|---|

| Mercury | $250 | Bonus via referral link |

| Ramp | $250 | Cash back available on card spend |

| Rho | $500 | Cash back varies by terms |

Traditional banks charge you $25/month and offer nothing in return. The math isn't close.

FDIC Insurance & Safety

"But are fintech banks safe?"

Yes. Fintech banks partner with FDIC-insured institutions. Your money is protected up to $250k per account (some offer extended coverage up to $6M through multiple partner banks).

Mercury partners with Choice Financial and Evolve Bank & Trust. Ramp partners with Customers Bank. Rho partners with Webster Bank. All FDIC-insured.

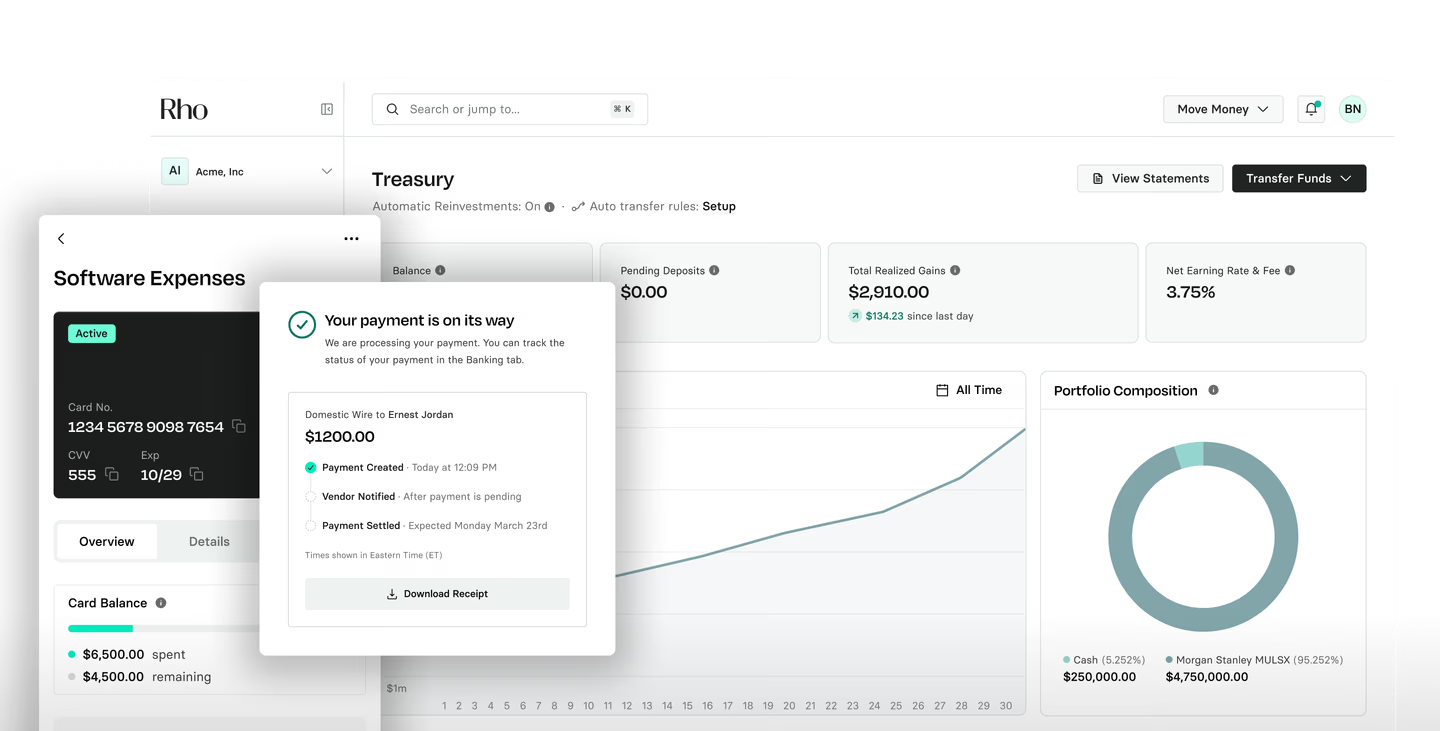

Treasury & Cash Management Rates (Operating Cash vs Higher-Yield Accounts)

As of February 22, 2026, here is the practical split: operating/checking/savings balances are usually more liquid and lower yielding, while treasury/investment balances can earn more but are managed as separate products with variable rates and different liquidity rules.

| Provider | Operating / Savings Rate | Treasury / Investment Rate | Liquidity Tradeoff |

|---|---|---|---|

| Mercury | Core operating account APY is not prominently published | Mercury Treasury: up to 3.71% net yield | Higher-yield options include same-day money market and 1-2 business day ultra-short treasury choices. |

| Brex | Core business account is positioned for operating cash; treasury is the yield-focused product | Brex Treasury: 3.35%-3.70% total treasury return (balance-tiered, based on Brex's support table as of 2/10/2026) | Yield applies to funds moved into treasury investments and varies with market rates and total balance. |

| Ramp | Ramp Business Account: up to 2.00% annual cash rewards | Ramp Investment Account: up to 4.02% (reported in Dec 2025 release notes) | Business account is simpler operating cash; investment balances target higher yield but are managed separately and rates move over time. |

| Rho | Rho Savings: 1.50% APY | Rho Treasury: up to 3.71% APY | Savings has transaction limits and settlement times; treasury is marketed for higher-yield cash management with no lockups. |

| Relay | Relay Savings: 0.91%-2.68% APY (plan-based) | No separate treasury/investment rate publicly highlighted | Generally more liquid operating + savings setup, but lower top-end yield than treasury-style products. |

| Novo | Novo Checking / Reserves: no APY publicly listed on product pages | No separate treasury/investment rate publicly highlighted | Primarily an operating-cash and budgeting setup, not positioned as a treasury-yield product. |

How to use this in practice: Keep operating cash where speed and workflow integration matter most, then move true reserve cash into treasury/investment products when yield justifies the added complexity and liquidity constraints.

Best Business Bank Accounts for Startups (Detailed Reviews)

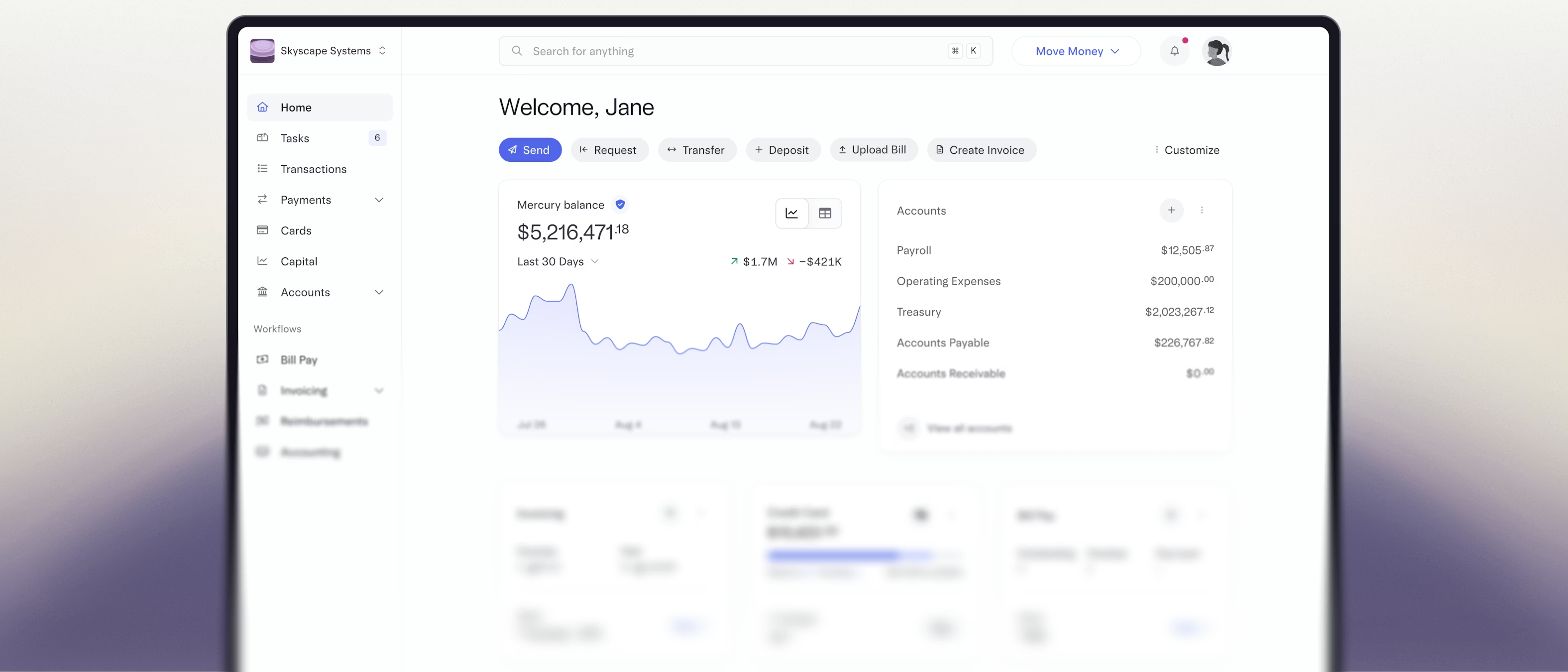

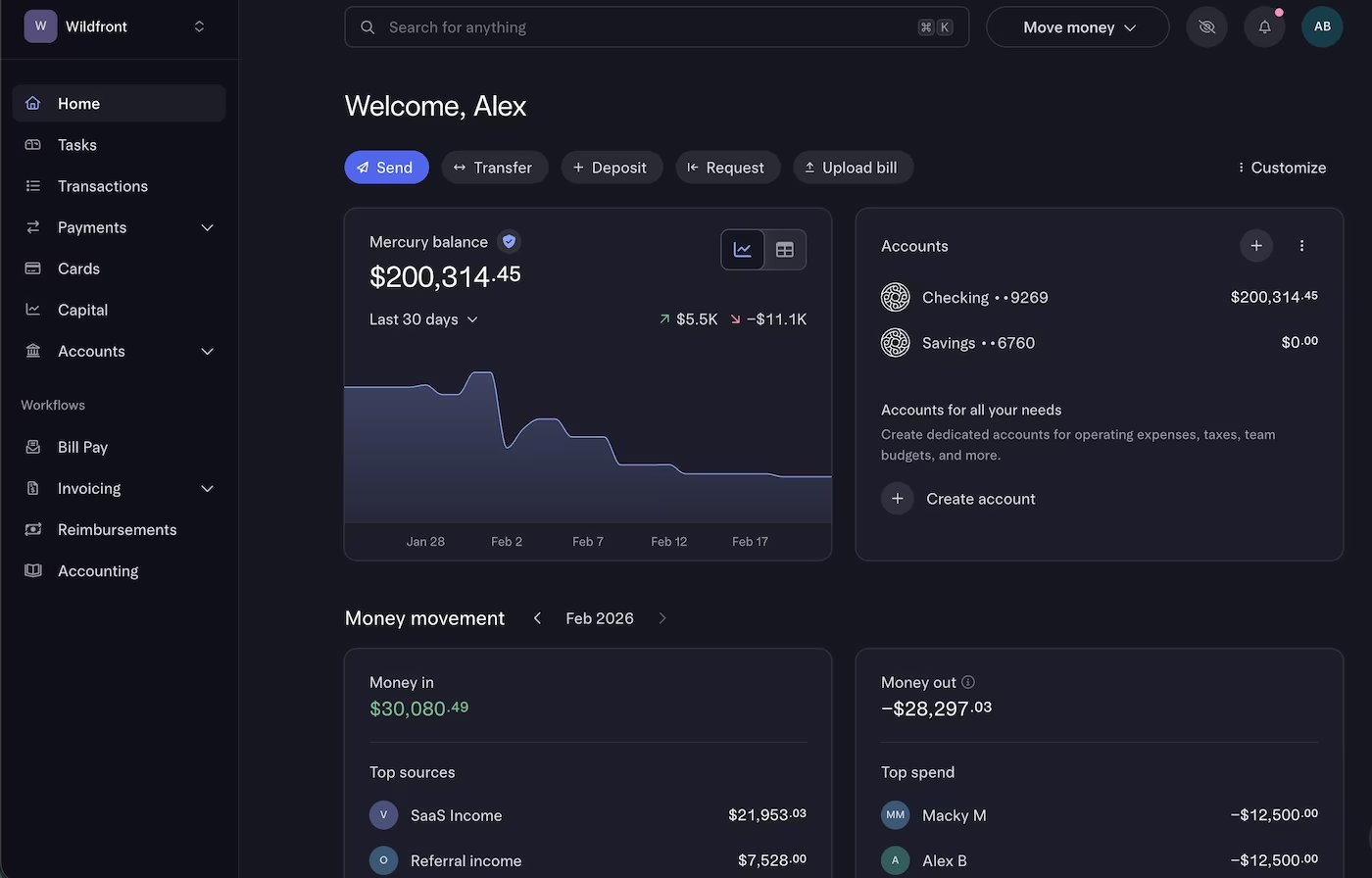

Mercury - Best Overall for Tech Startups

Mercury is the default choice for YC companies and tech startups. It's what happens when founders build a bank for founders—no branch visits, no stupid fees, just clean banking that integrates with your workflow and actually understands that negative cash flow isn't a problem when you have $2M in the bank.

| Metric | Details |

|---|---|

| Monthly Fee | $0 |

| Sign-Up Bonus | $250 (via referral link) |

| Setup Time | ~10 minutes |

| Best For | Tech startups, SaaS, VC-backed companies |

| Top Integrations | Stripe, QuickBooks, Gusto, Rippling |

| FDIC Insurance | Up to $5M through partner banks |

Why Mercury Works for Startups

The UI is genuinely good. Not "good for banking"—actually good. You can set up your account in under 10 minutes, issue virtual debit cards to your team instantly, and start accepting Stripe payments the same day.

Investor reporting: Mercury has built-in tools to share your dashboard with investors. Send burn rate, runway, and transaction summaries to your board without exporting CSVs. This alone saves hours per month if you're sending investor updates. Pair it with a SaaS financial model to track MRR, churn, and net income alongside your banking data.

Mercury Treasury: Automatically earn 4-5%+ on idle cash. If you're sitting on a $2M seed round, that's $90k/year in free money just from parking it correctly. Funds sweep into treasury overnight, sweep back instantly for payments. FDIC insured up to $5M through partner banks.

Credit without personal guarantee: Mercury offers credit lines based on your cash balance. If you have $500k in the bank, you might get a $100k line of credit with no personal guarantee. This is fundamentally different from traditional banks that want your house as collateral.

Drawbacks

Mercury is selective about industries. No crypto exchanges, cannabis businesses, or certain high-risk categories. If you're in a regulated or controversial space, you might get rejected.

No physical branches. In practice, that is usually fine because Mercury, Brex, Ramp, Rho, Relay, and Novo all offer mobile check deposit in-app for eligible accounts. The main reason to add a hybrid traditional bank is frequent cash deposits (not check deposits).

Bottom Line: If you're building a tech startup or SaaS company, Mercury is the default. Fast approval, clean UI, integrations with all the tools you use, and features designed specifically for venture-backed companies.

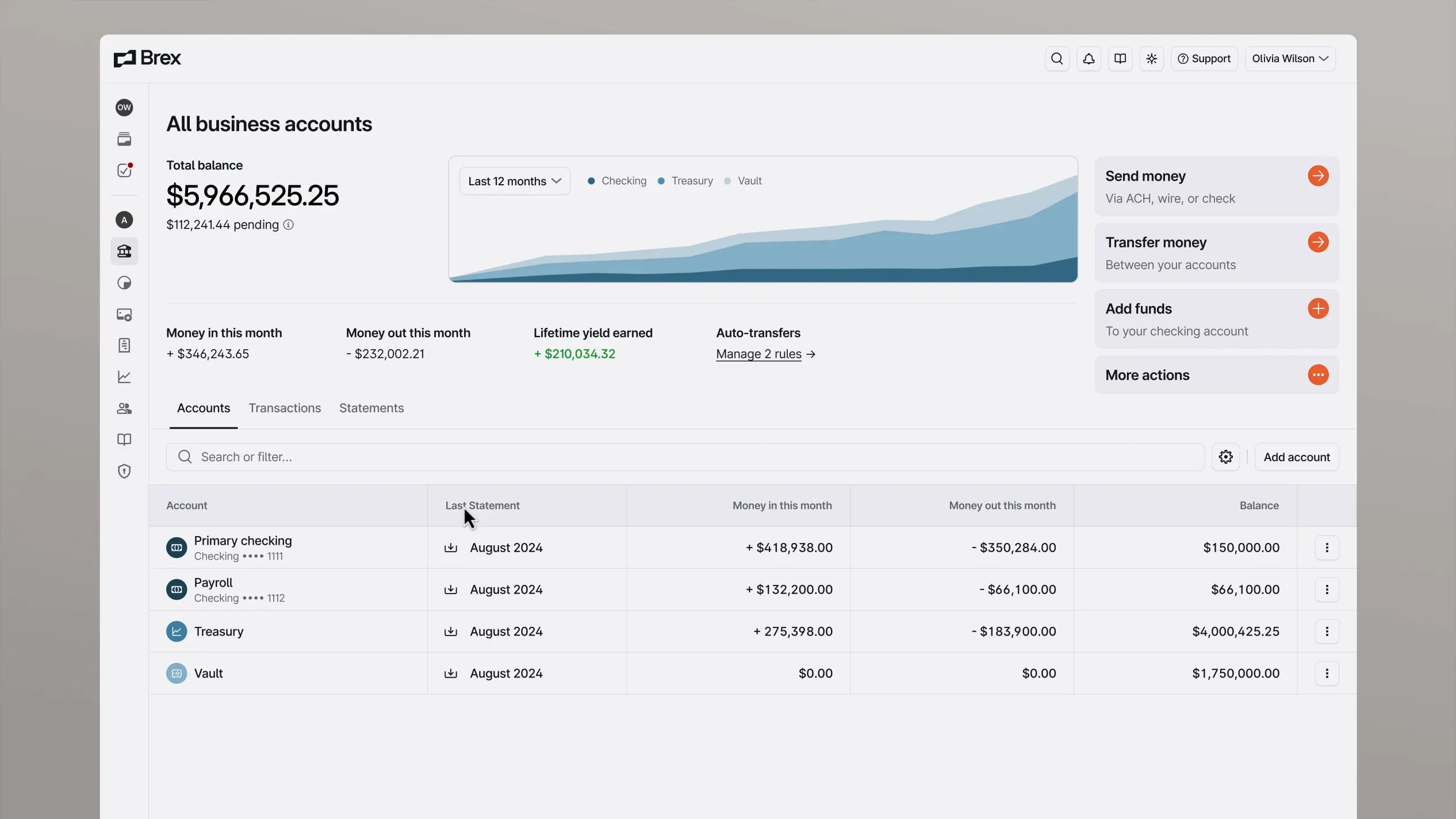

Get Mercury - $250 BonusBrex - Best for High-Spend Venture-Backed Startups

Brex is what you graduate to when your startup is spending $50k+/month and you need serious credit limits. They offer up to 40% of your ARR as a credit line without a personal guarantee, 1-7x points on categories like travel and software, and banking features built for scaling teams.

| Metric | Details |

|---|---|

| Monthly Fee | $0 (Premium: $49/mo) |

| Sign-Up Bonus | Points (varies) |

| Credit Options | Up to 40% ARR without personal guarantee |

| Setup Time | ~1 day |

| Best For | High-spend, venture-backed, scaling companies |

| Top Integrations | NetSuite, Xero, Rippling, Concur, Navan |

| FDIC Insurance | Up to $6M through partner banks |

Why Brex Works for Startups

Highest credit limits in the space: Brex approves credit up to 40% of your ARR or a percentage of your funding without a personal guarantee. If you're doing $1M ARR, that's potentially $400k in credit. Traditional banks won't even talk to you until you're profitable.

Premium rewards: 1-7x points depending on category. 7x on travel, 4x on software/SaaS subscriptions, 2x on advertising. If you're spending $20k/month on AWS, ads, and tools—including an outsourced sales team—the points add up fast. Redeem for travel, cash back, or statement credits.

Expense management: Brex has built-in receipt matching, policy enforcement, and approval workflows. Issue cards to your team with automatic spend limits. Receipts get matched automatically through AI. Finance team spends zero time chasing expense reports.

Travel perks: If your startup travels for conferences, customer meetings, or team offsites, Brex includes lounge access, travel credits, and concierge services. It's positioned as the "Amex Platinum for startups."

Drawbacks

Requires venture funding: Brex wants to see VC backing. If you're bootstrapped or pre-seed without institutional investors, you'll likely get rejected. They're explicit about targeting venture-backed companies.

Premium features cost money: The free tier is solid, but advanced features (custom rewards, priority support, higher limits) cost $49/month. Still cheaper than traditional banks, but not free.

Overkill for early-stage: If you're spending less than $20k/month, Brex is probably too much bank. Mercury or Relay makes more sense until you scale.

Bottom Line: If you're venture-backed, spending $50k+/month, and need serious credit limits without personal guarantees, Brex delivers. Premium rewards, expense automation, and credit terms designed for high-growth startups.

Get BrexBrex vs Mercury: Direct Comparison

Brex and Mercury are relatively similar solutions. Our experience from having accounts at both institutions is that Brex "feels" a little more awkward to use in all areas: the user experience (UX) of the technology itself takes some getting used to, whereas when you use Mercury for the first time, you'll likely just "get it" faster. This feedback applies to both the regular day to day use (moving money, paying bills etc) as well as the accounting sync (pushing pre-coded transactions to QBO/Netsuite). In most other ways, including cost-wise, they're highly comparable in the sense that both are startup-friendly e-banks that are free to use in most ways.

One notable addition here is that Brex was recently acquired by Capital One, so we'll have to wait and see if the experience changes (for better or for not-as-good!) post-acquisition. Brex has historically paid out better signup bonuses, though, if you're a smaller scale startup - honestly, you might as well open accounts with both places, try them both out, maximize your cash back bonuses, and decide for yourself.

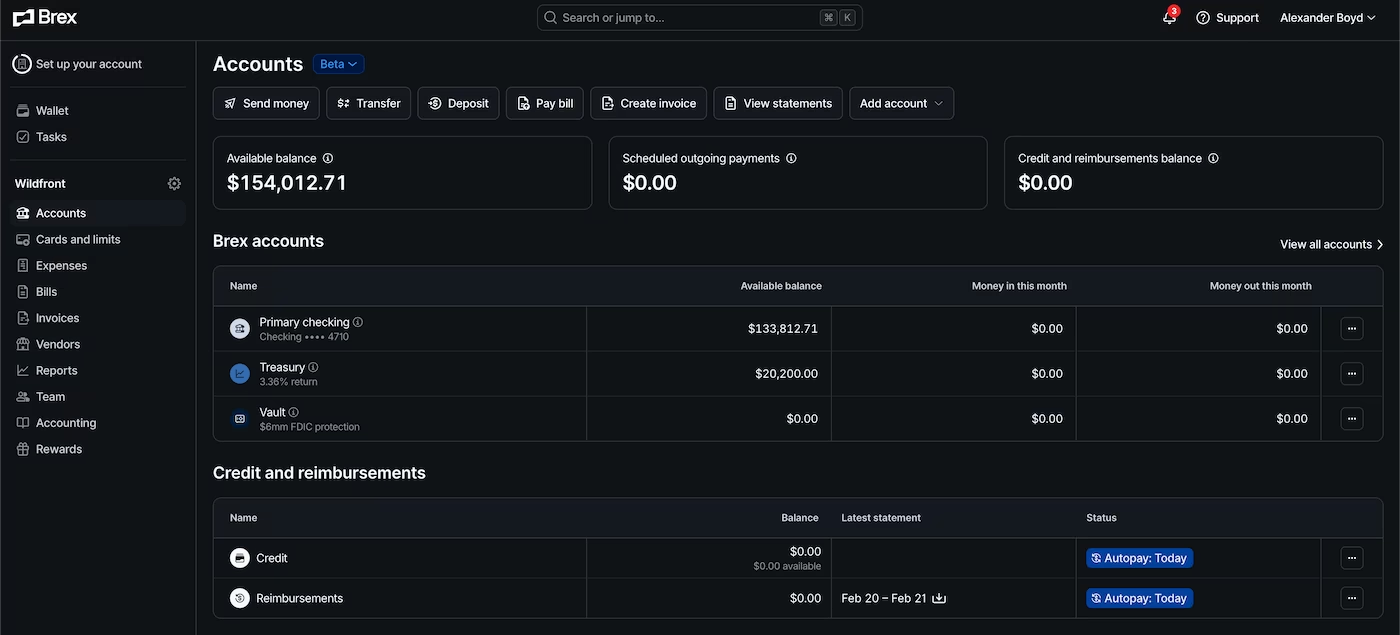

Ramp - Best for Expense Management & Cashback

Ramp is expense management on steroids with 1.5% cashback on everything. If you have a team making purchases and you're tired of chasing expense reports, Ramp automates the entire workflow—receipt matching, policy enforcement, approval chains—and pays you 1.5% for the privilege.

| Metric | Details |

|---|---|

| Monthly Fee | $0 |

| Sign-Up Bonus | $250 |

| Cashback | 1.5% average on card spend |

| Setup Time | ~15 minutes |

| Best For | Teams, expense management, high spend |

| Top Integrations | NetSuite, Sage, Xero, QuickBooks |

| FDIC Insurance | Up to $250k (Customers Bank) |

Why Ramp Works

Think of Ramp as your CFO's best friend. Every purchase automatically matches receipts. Spending controls let you set limits per employee or card. Bill pay automation saves hours every month. And you earn 1.5% cashback on everything.

The accounting software integrations are exceptional—NetSuite, Sage Intacct, Xero, QuickBooks all sync in real-time. If you're tired of manually categorizing expenses or chasing down receipts, Ramp fixes that.

Real Example: If your LLC spends $10,000/month on expenses, you'll earn $150/month = $1,800/year in cashback + $250 sign-up bonus. That's $2,050 in year one versus $0 from traditional banks.

Bottom Line: Best choice for LLCs with teams, significant expenses, or anyone who wants to automate spend management while earning cashback.

Get Ramp - $250 Bonus + 1.5% CashbackRho - Best for Finance Operations + Highest Bonus

Rho combines business banking, corporate cards, AP automation, and treasury management into one platform—and they'll pay you $500 to open an account. If you have a finance team (or plan to build one), Rho replaces 3-4 tools with a single integrated system.

| Metric | Details |

|---|---|

| Monthly Fee | $0 |

| Sign-Up Bonus | $500 (highest available) |

| Cashback | Variable on card spend |

| Setup Time | 1-2 days (requires revenue) |

| Best For | Growth-stage LLCs, AP/AR automation |

| Top Integrations | QuickBooks, Xero, NetSuite, Bill.com |

| FDIC Insurance | Up to $250k (Webster Bank) |

Why Rho Works

Rho targets established LLCs with real revenue and vendor relationships. You get corporate cards, AP automation, bill pay workflows, and treasury management in one platform. Multi-entity support is exceptional if you run multiple LLCs.

The vendor payment workflows alone save hours every month. Advanced reporting gives you real-time visibility into cash flow. And the treasury features help you maximize yields on idle cash.

The catch? Rho requires business revenue—they're not accepting brand-new LLCs. Approval takes 1-2 days versus instant. This is overkill if you just need simple banking.

Bottom Line: Best for established LLCs with revenue, vendor relationships, and finance operations that need automation. The $500 bonus and multi-entity support are unmatched.

Note About Rho Referral

To claim the $500 Rho sign-up bonus, contact us for a referral. We'll connect you directly to ensure you receive the full bonus.

Comparison by Use Case

Best for Brand New LLCs (Just Filed)

Top Pick: Mercury or Novo

You just filed your LLC and need an account fast. Mercury approves in ~10 minutes with just your EIN and Articles of Organization. Novo is equally fast and even simpler.

Best for Tech Startups & SaaS

Top Pick: Mercury

Mercury was built specifically for this use case. Investor update tools, cap table integrations, and a founder-friendly interface make it the default choice for tech startups.

If you're running high transaction volume, both Mercury and Rho are strong fits: Mercury keeps day-to-day payments and reconciliations fast, while Rho adds deeper AP workflows and finance controls as volume scales.

Best for E-Commerce LLCs

Top Pick: Ramp or Relay

E-commerce businesses benefit from Ramp's cashback (1.5% on inventory, ads, software) or Relay's multiple accounts (separate inventory, operations, tax funds).

Best for No-Fee Banking

Top Pick: Mercury

Every bank we recommend charges $0/month. Compare that to traditional banks:

| Bank | Monthly Fee | Annual Cost |

|---|---|---|

| Chase Business Checking | $15-25 | $180-300 |

| Bank of America Business | $16-29.95 | $192-359 |

| Wells Fargo Business | $14-40 | $168-480 |

Savings over 5 years: $900-2,400 by avoiding traditional banks.

How to Open a Business Bank Account for Your LLC

What Documents You'll Need

- EIN (Employer Identification Number) - Get it free from IRS.gov, takes 5-10 minutes online

- Articles of Organization - Your LLC formation documents from your state

- Operating Agreement - Some banks require this, others don't

- Government-Issued ID - Driver's license or passport

- Business License (if applicable) - Some industries require state/local licenses

Step-by-Step Process

- Get Your EIN - Visit IRS.gov and apply online. Free, takes 5 minutes, you get it immediately.

- File Your LLC - File with your state. You'll receive your Articles of Organization.

- Create an Operating Agreement - Even if your state doesn't require it, create one.

- Choose Your Bank - Use this guide to pick the right fit.

- Apply Online - All the banks we recommend have online applications. Takes 10-30 minutes.

- Verify Your Identity - Upload your ID and documents. Most banks verify instantly.

- Fund Your Account - Initial deposit requirements vary ($0-100 typically).

- Get Your Debit Card - Physical cards arrive in 1-2 weeks. Virtual cards available immediately.

- Set Up Integrations - Connect Stripe, QuickBooks, payroll providers, etc.

Cash Back & Sign-Up Bonuses: Free Money for Your LLC

Traditional banks charge you fees. Modern banks pay you bonuses. The difference is wild.

Sign-Up Bonus Comparison

| Bank | Sign-Up Bonus | Requirements | Timeline |

|---|---|---|---|

| Rho | $500 | Open account, meet deposit/spend requirements | 60-90 days |

| Mercury | $250 | Open account via referral link | 30-60 days |

| Ramp | $250 | Open account, activate card | 30-60 days |

Strategic Approach: Stack Your Bonuses

Smart founders don't choose just one bank. They stack benefits:

- Open Mercury for primary banking, treasury, integrations → Get $250 bonus

- Open Ramp for corporate card/expense management → Get $250 bonus + ongoing 1.5% cashback

- Open Rho (if needed for AP automation) → Get $500 bonus

Total first-year bonuses: $1,000 + ongoing cashback from Ramp.

There's no limit to how many business bank accounts your LLC can have. Opening multiple accounts to maximize bonuses is perfectly legitimate (and smart).

FAQ: Business Bank Accounts for LLCs

Do I legally need a separate business bank account for my LLC?

Technically, it depends on your state. Practically: YES, absolutely.

Here's why:

- Maintain your corporate veil protection - If you commingle personal and business funds, you risk "piercing the corporate veil." This means a court could hold you personally liable for business debts.

- Easier bookkeeping and taxes - Separate accounts make it simple to track business income and expenses.

- Professional appearance - Accepting payments and issuing checks from "Smith LLC" looks more professional.

- Required for accepting payments - Payment processors like Stripe require business accounts for business entities.

- IRS audit protection - Clean separation between personal and business finances makes audits smoother.

Bottom line: Get a business bank account the day you file your LLC.

Can I use a personal bank account for my LLC?

You can, but you shouldn't. Using a personal account for LLC transactions risks:

| Risk | Why It Matters |

|---|---|

| Pierced corporate veil | Loss of liability protection |

| Tax complications | Harder to document business deductions |

| Payment processor violations | Stripe and PayPal require business accounts |

| Professional credibility | Less trust with vendors and customers |

Plus, business accounts are free now. Mercury, Ramp, Rho, Relay, and Novo all charge $0/month. There's no cost benefit to using a personal account anymore.

How much does it cost to open a business bank account for an LLC?

Fintech banks: $0

| Fintech Bank | Monthly Fee |

|---|---|

| Mercury | $0 |

| Ramp | $0 |

| Rho | $0 |

| Relay | $0 |

| Novo | $0 |

Traditional banks: $0-100 initial deposit, plus monthly fees

| Traditional Bank | Initial Deposit | Monthly Fee |

|---|---|---|

| Chase | $0 | $15-25 |

| Bank of America | $25-100 | $16-29.95 |

| Wells Fargo | Varies | $14-40 |

Bottom line: Opening an account is free everywhere. The difference is ongoing fees—fintech banks charge $0/month forever.

What credit score do I need for a business bank account?

Good news: Most fintech banks don't check personal credit for business checking accounts.

Mercury, Ramp, Rho, Relay, and Novo focus on:

| Focus Area | What They Evaluate |

|---|---|

| Business legitimacy | EIN, Articles of Organization |

| Business model | Industry, revenue, plans |

| Identity verification | Owner and entity verification |

Your personal credit score typically doesn't matter for basic business checking.

What About S-Corps?

Can S-Corps Use These Banks Too?

Yes! If your LLC elected S-Corp tax status, you can (and should) use these same business bank accounts.

Quick Explainer: What's an S-Corp Election?

An S-Corp isn't a business structure—it's a tax designation.

Key points:

| Point | What It Means |

|---|---|

| Still an LLC | No new formation documents required |

| IRS election | File Form 2553 for S-Corp tax treatment |

| Tax savings | Common for profitable LLCs to reduce self-employment taxes |

| Owner pay | Pay a reasonable salary, then take distributions |

Best Banks for LLC Taxed as S-Corp

1. Mercury - Gusto integration makes payroll seamless

2. Ramp - Expense categorization helps with S-Corp compliance

3. Rho - Advanced finance ops useful as S-Corp complexity grows

Bottom Line: If you're an LLC taxed as an S-Corp, use the same bank recommendations. Just prioritize those with strong payroll integrations (Mercury + Gusto is a popular combination).

Banks to Avoid (or When Traditional Banks Make Sense)

Traditional Banks You Can Skip for Most LLCs

For 90% of LLCs (especially tech, SaaS, e-commerce, service-based), fintech banks are objectively better.

Traditional banks made sense in 2015. In 2026, there's no compelling reason to pay $25/month for worse service, slower support, and limited integrations.

Legitimate Reasons to Choose a Traditional Bank

- Frequent cash deposits - If you're running a retail store, restaurant, or cash-heavy business

- SBA loans - If you need immediate access to SBA 7(a) or 504 loans

- International wire compliance - Some traditional banks have better international banking relationships

- In-person support - If you genuinely prefer face-to-face banking

The Hybrid Approach

Many smart founders use both:

Primary operating account: Mercury or Ramp (daily banking, integrations, $0 monthly fees)

Secondary traditional account: Chase or BoA (SBA loan access when needed, cash deposits if applicable)

Traditional Banks vs. Fintech Banks: Quick Comparison

When to Choose Fintech Banks

Choose fintech if:

| Situation | Why Fintech Wins |

|---|---|

| Tech, SaaS, e-commerce, or service business | Better integrations and workflows |

| Cost-sensitive operations | Saves $180-480/year in fees |

| Modern tool stack | Stripe, QuickBooks, and payroll sync |

| No need for physical branches | All-digital onboarding and support |

| Need automation | Virtual cards, rules, and controls |

The Reality in 2026

90% of LLCs should use fintech banks. The cost savings alone ($180-480/year) plus sign-up bonuses ($250-500) make the math obvious.

Best strategy: Primary account at Mercury/Ramp (daily operations), secondary account at Chase/BoA (if you need cash deposits or SBA loans).

Conclusion: Best Business Bank Accounts for Your LLC

TL;DR Recommendations

🏆 Best Overall: Mercury

Tech startups, SaaS, most LLCs. Clean banking, zero fees, $250 bonus, best integrations.

Get Mercury - $250 Bonus →

💳 Best for Expense Management: Ramp

Teams, high spend, expense automation. $250 bonus + 1.5% cashback on everything.

Get Ramp - $250 Bonus + 1.5% Cashback →

🏦 Best for Finance Ops: Rho

Established LLCs, AP automation, multi-entity. $500 bonus (highest available).

Contact Us for Rho Referral - $500 Bonus →

Action Steps

- Get your EIN (if you haven't already) - Visit IRS.gov, apply online, takes 5 minutes, free.

- Choose your bank based on your LLC type - Tech/SaaS → Mercury, Teams/expenses → Ramp, Established/finance ops → Rho

- Apply online (takes 10-30 minutes) - All applications are digital, no branch visits required.

- Set up integrations - Connect Stripe, QuickBooks, Gusto, etc.

- Start banking like a real business - Separate personal and business finances immediately.

Final Thought

Your business bank shouldn't cost you money or slow you down.

In 2026, there's zero reason to pay Chase $25/month for worse service when Mercury, Ramp, and Rho offer better products for free—and pay you up to $500 just to open an account.

Traditional banking made sense when it was the only option. It's not anymore.

Choose the bank that fits your LLC's needs, pocket the sign-up bonuses, and spend that $300/year you would've wasted on bank fees on literally anything else.

Affiliate Disclosure: This article contains affiliate links. If you open an account through our links, we may earn a commission at no cost to you. We only recommend banks we genuinely believe are the best options for LLCs.

Join a room of bootstrapped SaaS founders

Wildfront+ is an invite-only mastermind of vetted founders — professionally facilitated calls, honest feedback, no fluff. Or start free with the bootstrapper academy.